As Mexico Votes, State Oil Company Pemex Needs a New Direction

In less than two weeks Mexicans will vote for their next president. The outgoing leader, Andrés Manuel López Obrador, has made energy sovereignty and self-sufficiency one of the sustained themes of his presidency. AMLO, as he is universally known, has focused his energy aspirations on Pemex, the world’s most indebted national oil company. What Mexico’s next president does with Pemex will determine the country’s energy and fiscal future amid a rapidly changing outlook for fossil fuels.

Pemex faces unprecedented risk brought about by the quickening global energy transition away from hydrocarbons. At NRGI, we have described that risk in a new Spanish-language report, and summarize it below. We also offer some recommendations for the victor in June’s elections and the Pemex executives, including its director, whom the new president will appoint.

A risky business

National oil companies (NOCs) account for 55 percent of the world's oil production and yet they are moving more slowly than their private sector counterparts in terms of decarbonization planning.

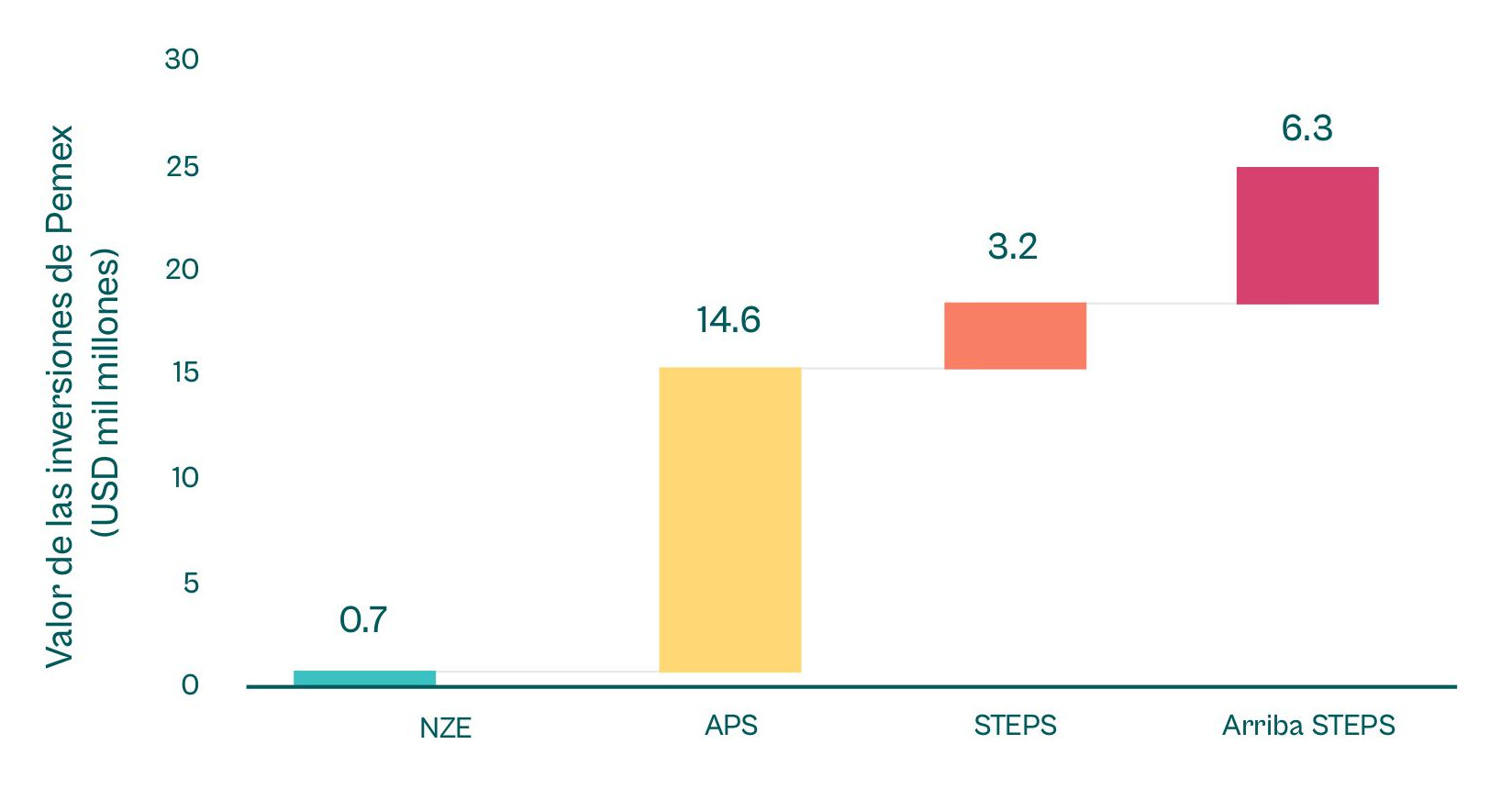

Among the 58 NOCs we studied last year, Pemex ranked 11th in terms of its exposure to transition risk. The biggest of these risks is the changing economics of the oil sector, with demand likely to markedly diminish in coming decades as countries seek to meet their emissions reduction goals. Mexico’s remaining oil reserves will be increasingly costly to extract, meaning that as global oil prices fall, Pemex may be caught out, its assets “stranded.” We found that approximately $10 billion in Pemex's expected investment over the coming decade would not break even under the IEA’s Announced Pledges Scenario for future oil demand. Given Pemex’s already problematic debt obligations, this presents the government with the specter of more bailouts to alleviate the company’s financial situation, generating an even deeper crisis.

Value of Pemex's upstream oil and gas investments breaking even in each of the IEA's scenarios.

In late 2022, Pemex presented a new business plan which, for the first time, explicitly referenced the energy transition. The plan recognized as risks the international hydrocarbon market contraction due to the increase in electric vehicles, and the downward trend in the demand for oil-derived plastics. While this recognition was an important first step, we still know little about what government officials and Pemex executives plan to do with respect to the transition.

In March 2024 Pemex released a sustainability plan that included more detail on some aspects of its intentions to reduce production emissions. But the plan did not address the transition risk in terms of falling global demand and prices.

Early dissemination of our findings in a workshop with climate and energy experts in Mexico yielded more insight:

- Pemex’s diversification plans remain somewhat vague, and their technical feasibility is uncertain.

- Pemex must be more transparent and accountable about its financial situation.

- Many sector insiders believe that the transition will be slow, and that Pemex will remain competitive.

We are confident that experts from Mexico’s oil and gas sector and its climate community can work with Pemex to improve understanding and communication of its plans.

How to improve Pemex’s future

Our research and consultations have led us to propose three categories of recommendation:

1. Pemex should further recognize and analyze transition risks.

This means more thorough scenario planning around market conditions, shared publicly. And Pemex officials should include more acknowledgement of transition risk in their financial reporting—not just in planning.

2. Pemex should adopt and adapt transition risk mitigation approaches from other oil companies.

Executives should look very carefully at large fields with high production costs. Factoring in lead times (7.5 years on average) and changing market conditions, these may not represent the bonanza that some imagine. One such find is the Kante field in Tabasco state; our analysis suggests that increased investment could be a financial misstep. Ambitions around producing more “no matter what” should give way to innovative thinking about Pemex’s potential role in a domestic energy transition.

Regarding diversification and downstream activities, executives have several opportunities. First, Pemex should better coordinate with CFE, Mexico’s state-owned electricity company. Both can play a fundamental role in advancing the energy transition. Leadership should build a coordinated and integrated vision and action plan that defines the role of each company.

Decision-makers must also carefully consider the viability of diversification options. For example, the two leading presidential candidates have been enthusiastic about expansion in petrochemical production. But petrochemicals only account for 12 percent of current oil demand and the global market may soon be oversupplied as many oil companies seek to expand. This presents a risk of overinvestment and therefore warrants caution.

3. Mexico’s next president should oversee key changes in the government’s approach to the oil and energy sectors.

Mexico’s energy ministry (SENER) should assume a transition planning role in which officials consider the transition risk and build synergies among the country’s state-owned energy companies.

Meanwhile, the finance ministry (SHCP) should review the conditions for financial support to Pemex in the interest of fiscal responsibility and transparency in the management of public resources.

Moreover, the state, as Pemex’s owner, has a crucial role in holding the company accountable. SENER, SHCP, the Congress of the Union and the Federal Superior Audit Office determine and supervise the company's ownership policy. These actors should therefore play a role in improving transition-related decision making within Pemex.

Whoever triumphs on 2 June must stop Pemex from making risky bets and have a clear vision for the company—and Mexico—in a world in transition.

Mexico’s risky bets

Learn more about the transition risks Pemex faces with new NRGI research.

Authors

Fernanda Ballesteros

Mexico Country Manager

Andrea Furnaro

Policy Analyst