One Tax to Rule Them All: A Variable-Rate Royalty Might be More Effective with Volatile Extractive Prices

In the last decade, governments of resource-rich countries like Zambia, Guinea and Mongolia have struggled to tax their extractive industries more effectively. It is a tall order—countries must design an inescapable tax regime that taxes companies more in times of high profits and allows some relief in periods when gains are low. Few nations have found a perfect solution. The Democratic Republic of Congo is now facing this challenge, as officials review the DRC’s mining code at the bottom of the commodity cycle. With a strong opposition from the DRC Chamber of Mines to a new proposed fiscal package, should DRC look into a price-based royalty?

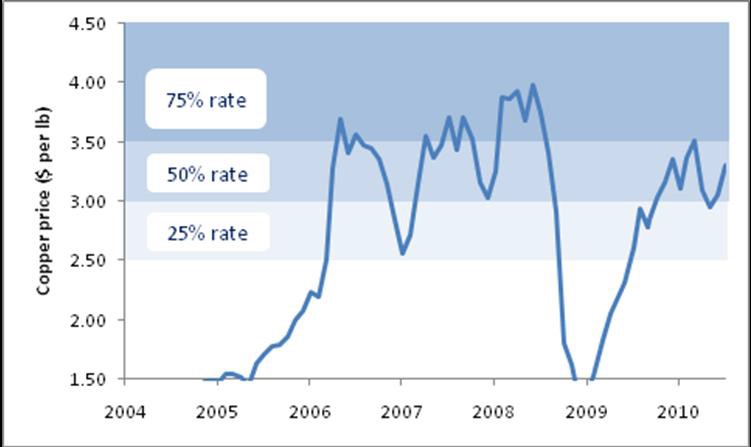

Not long ago, authorities in Zambia thought that a “price-based royalty” could be a solution to their dilemma. (In Zambia it was called a “windfall tax.”) This tax is based on a measure of gross sales revenue with a rate that automatically varies according to the average price of a commodity. The price-based royalty in Zambia has three marginal rates based on the three thresholds of the London Metal Exchange copper price.

Figure 1. The three price thresholds determining the marginal rate of Zambia’s price-based royalty

Source: David Manley. “A guide to mining taxation in Zambia.” Zambia Institute for Policy and Research, June 2013.

This tax is relatively easy to administer, compared to a profit-based tax—an authority need only calculate gross revenue and average mineral prices, not the actual costs of extraction, transport and refining. (Authorities still need to be able to monitor production and sales.) It is also somewhat sensitive to a company’s profitability, if we assume that a rise in the copper price will increase a company’s profits. But this is a questionable assumption, upon which rests the legitimacy of a price-based royalty. The long, drawn-out fights between the government and mining companies in Zambia have shown that the debate can be fierce. Zambia’s windfall tax only lasted a year before the government in 2009 capitulated in the face of a lobbying onslaught. The companies argued that the price-based royalty was not sensitive to changes in profit and would drive them out of business. Specifically, they argued that their costs were much higher than the Zambian authorities had assumed.

Other countries’ experiences also highlight the possible flaws in a price-based royalty. Mongolia and Guinea both had simple price-based royalties whose rates would increase when the price of gold rose above USD 500 per ounce. This threshold was quickly passed in the recent gold boom and the price of gold has remained above USD 1,000 since 2009. However, few analysts would argue that the gold industry is currently enjoying windfall profits—extraction costs have ballooned in the meantime.

A key question, therefore, is how closely oil, gas and mining profits track with commodity prices. If there is a strong correlation, then price-based royalties are reasonable replacements for excess profit taxes. If not, then policymakers should look to alternative instruments to tax extractive resources while making sure their countries remain attractive jurisdictions for investors.

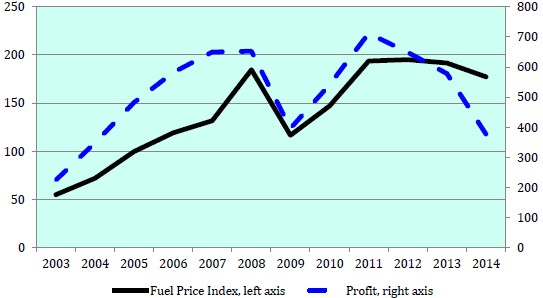

In their October International Centre for Tax and Development research paper, Kimberly Clausing and Michael Durst provided some guidance. They found that for a 1 percent rise in oil and mineral prices, oil company profits rise by 0.76 percent and mining company profits rise by 1.38 percent. Figure 2 shows their result for the global oil market, in which oil company profits loosely track with the oil price.

Figure 2. Average profits of oil and gas firms (in million USD) and the Fuel Price Index

Source: Kimberly Clausing and Michael Durst. “A price-based royalty?” ICTD Working Paper 41, October 2015.

In an OxCarre research paper, Gerhard Toews and Alexander Nuamov explored the relationship between oil prices and industry expenditures and find that costs increase or decrease less than proportionally with prices. This implies that increased prices do increase profits, which, along with Clausing and Durst’s results, should give more support to the use of price-based royalties. Although it is not clear how closely profits need to move with prices for a price-based royalty to be viable for most extractive companies. Is a profit change of 0.76 percent enough, for instance? Plugging these numbers into a model and experimenting with various price-based royalty designs might yield some interesting results and could be a useful next step.

Thomas Lassourd and David Manley are economic analysts at the Natural Resource Governance Institute (NRGI).

Authors

David Manley

Lead Economic Analyst – Energy Transition