Mexico as a “Re-Exporter” of U.S. Gas: How Real Are the Prospects?

“Re-exporting” U.S. gas through Mexico has become a hot topic in political and energy circles. The basic idea is this: U.S.-based companies would pipe gas from Texas’s Permian Basin to new export facilities on Mexico’s Atlantic and Pacific coasts, where it would be liquefied and shipped abroad.

Influential voices in both countries now back this model, and recent statements from both governments suggest that building new liquefied natural gas (LNG) export infrastructure in Mexico is a priority on the bilateral agenda. But how realistic are these plans, given current global LNG markets and possible opposition and delays inside Mexico? And does it make sense for Mexico to deepen its already risky dependence on U.S. gas?

Big ambitions

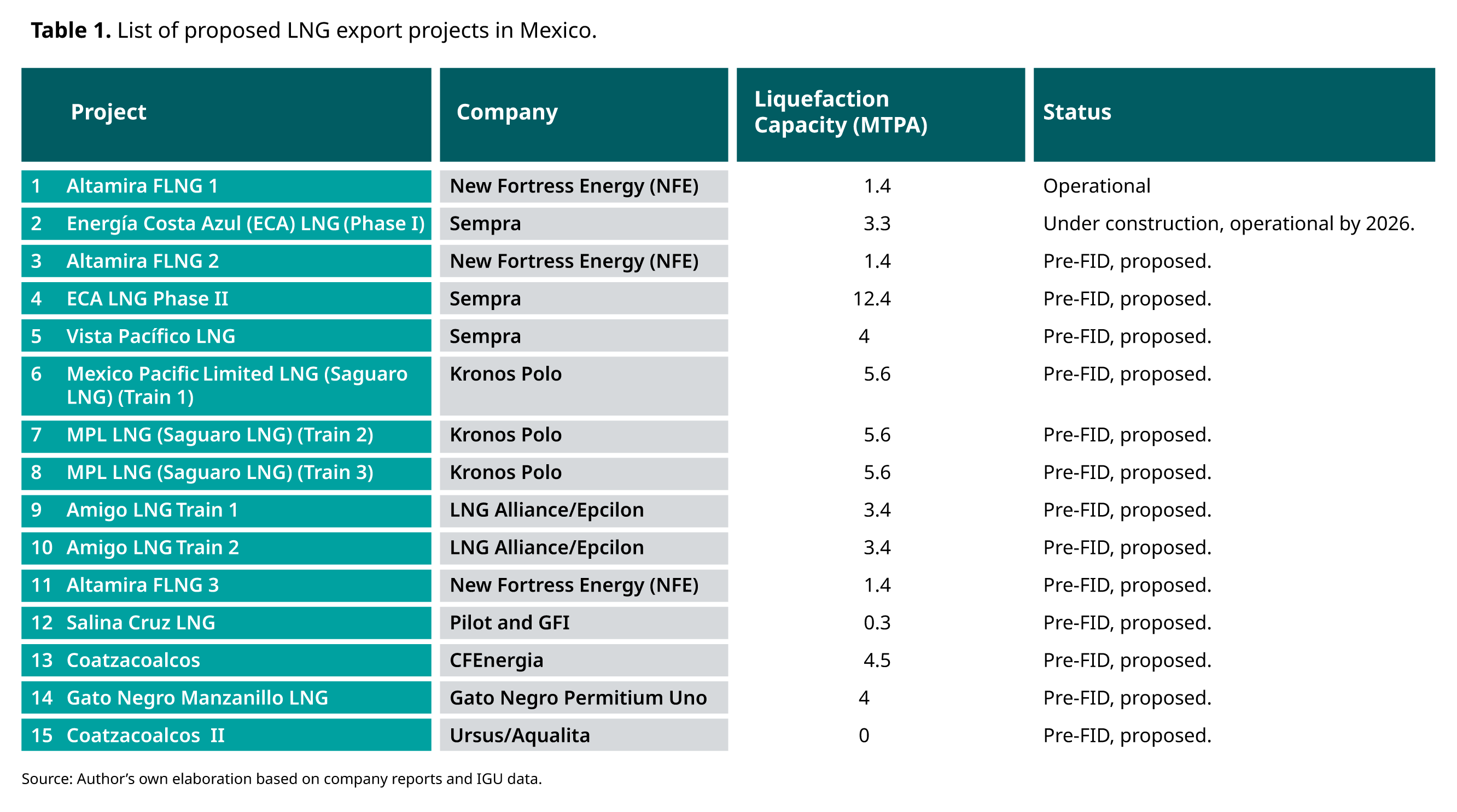

Private companies and investors, many of them based in the U.S., want to build as many as fifteen new gas liquification plants in Mexico that, on paper, could supply a tenth of the world’s LNG. In practice, however, this seems highly optimistic, given financial constraints, uncertainty over the medium- and long-term outlook of global demand for LNG, and opposition from communities in Mexico, among other challenges.

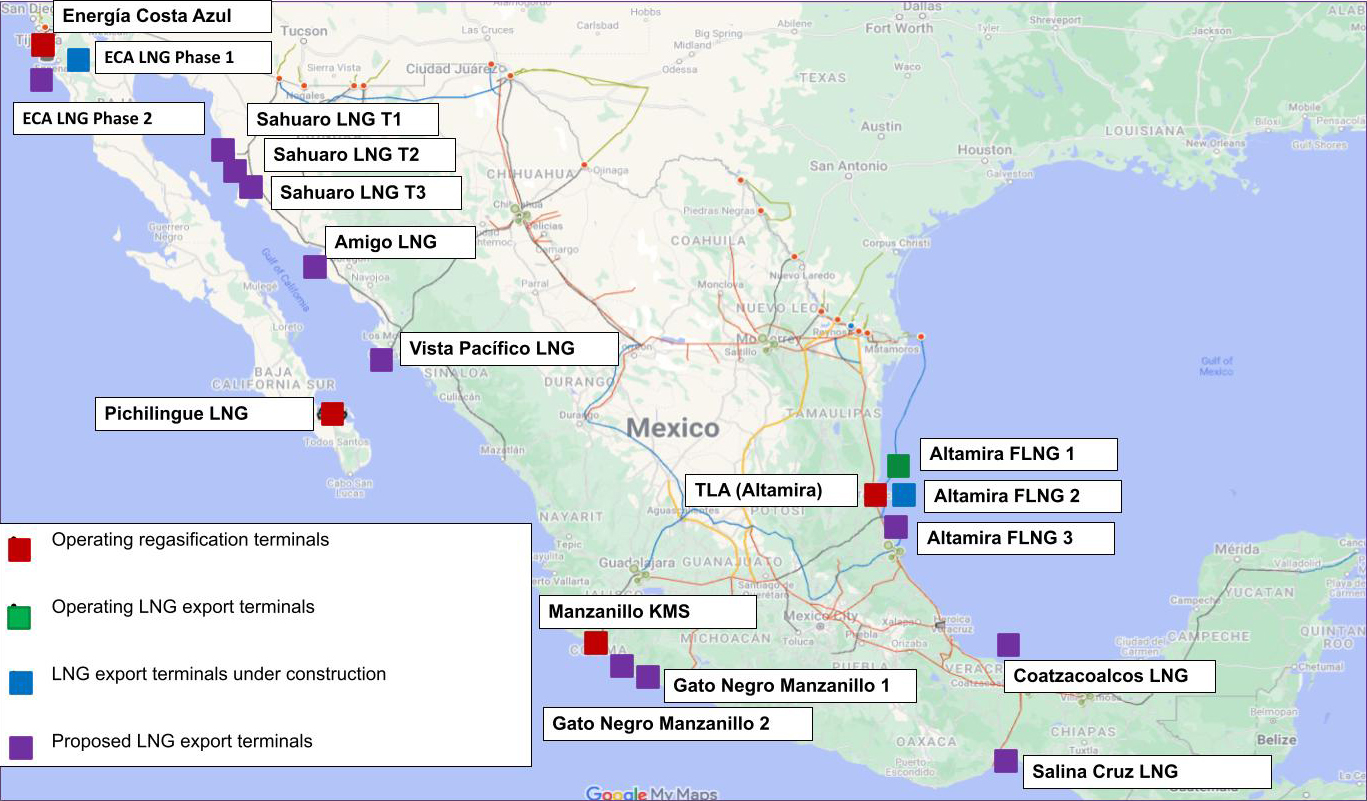

These proposals mirror the frenzy of U.S. LNG announcements over the past decade, of which only a fraction were or will be built. As of today, just two Mexican projects have moved forward. One small plant, Altamira FLNG 1, is operating on the Atlantic side, while a second, ECA LNG, is under construction on the Pacific coast. None of the other projects have reached final investment decision (FID). A couple have signed long-term gas sale agreements—an important step, but no guarantee of success.

Uncertain demand

While it is impossible to predict how many, or which, projects will go ahead, many could struggle to find buyers for their gas. The Atlantic coast plants would ideally sell to buyers in Europe, but demand there is shaky and Mexican projects face strong competition from existing and future U.S. terminals that would benefit from lower pipeline shipping costs. Notably, Altamira FLNG1, Mexico’s only operating Atlantic facility, has yet to secure any long-term customers.

Gas shipped from the Pacific coast could have a competitive edge in reaching Asia-Pacific markets, which are expected to drive global demand for LNG. This advantage comes mainly from shorter shipping distances and the ability to avoid chokepoints such as the Panama and Suez canals. However, Mexico’s proximity to large Northeast Asian importers—Japan, China and South Korea—may not be as advantageous as it seems, since their LNG demand is likely to plateau or shrink in the 2030s. The outlook is also mixed in other Asian countries such as India, Pakistan or Vietnam, which are closer to rival producers like Australia or Qatar, and are rapidly pivoting to renewables.

So much to build

Even if demand for Mexican re-exported LNG were robust, companies would struggle to build the infrastructure needed. Pipelines within Mexico are a particularly complicated problem since existing ones from the U.S. cannot meet both domestic power demand and supply most of the proposed export terminals. New lines would need to stretch hundreds of kilometers through tough terrains, including areas with highly complex topography, protected national parks or controlled by drug cartels.

And crucially: will stakeholders in Mexico even allow these projects to be built? Strong social and legal opposition has also stalled pipeline projects in Mexico, some by nearly a decade. LNG terminals could encounter similar pushback, especially if they impact vulnerable populations and ecosystems. A court has already blocked construction of one large Pacific coast project, Saguaro LNG, after five separate lawsuits alleged constitutional, property, human rights, environmental and permitting abuses.

The clock is ticking

All this comes as LNG projects worldwide face serious time pressures. LNG companies plan to boost liquefication capacity by 40 percent by 2030, even though demand is growing by only two percent a year. Under Donald Trump, the U.S. especially is racing ahead, with LNG production up almost 20 percent year-on-year and with five export terminals accounting for over 50 million tons per annum reaching FID. With this, 2025 is already the second-highest year for LNG FIDs on record, behind only 2019. Add to this Washington’s decision to lift the moratorium on new LNG projects, which could help unlock more capital.

A global supply glut looks increasingly likely—bad news for Mexico’s LNG re-export ambitions, most of which lack concrete timelines. Meanwhile, rival plants in Canada are closer to opening, while Mexican ones are running years behind. At this point, it seems unlikely that any pre-FID projects will ship gas before 2030. The search for funding remains active—but how much of it will come too late, or never?

Separating true potential from hype

Assessing the real prospects for Mexican LNG “re-exports” is difficult in part because accurate, public available information is scarce. The Sheinbaum administration, for instance, has yet to clarify the role it envisions for these projects in Mexico’s economic and energy future, including how they could affect gas availability and prices for Mexican power plants and other consumers. This is a critical omission, given that Mexico’s dependence on U.S. gas already poses risks to energy security and costs.

Going forward, policymakers and companies should disclose much more data on the expected costs, timelines and impacts of planned LNG re-export projects. Without more information, the public cannot have the robust debate that is needed about whether becoming a middleman for U.S. LNG is truly in Mexico’s interests.

At NRGI, we will continue to engage with this important issue, including by offering recommendations on how transparency and accountability should improve. Our next post, out next month, will weigh the costs and benefits of betting big on re-exported gas.