Ghana’s Transition Minerals: No Time to Lose

The government of Ghana launched its energy transition framework in November 2022 at the COP27 climate conference in Egypt. The plan is to guide the country’s transition plans and map its resource needs for the coming 50 years. With global demand for oil anticipated to fall, Ghana’s oil revenues will soon begin to decline. That will have a direct impact on the government’s domestic revenues and subsequently on spending on critical areas such as healthcare, education and social protection. The oil sector contributes approximately 16 percent annually to Ghana’s domestic revenue and 4 percent to its GDP and absorbs a further 30,000 of the country’s labor force through direct, indirect and induced employment opportunities. But Ghana’s future is not in oil.

An aging fiscal regime

Graphite and lithium (recently discovered in large quantities in Ghana) are critical for the energy transition beyond fossil fuels, as these minerals are crucial inputs to green technologies. Ghana’s energy transition framework identifies graphite and lithium as future opportunities for state revenue.

But while Ghana’s fiscal regime includes revenue management laws specific to the waning oil sector, it has no such revenue management provisions for mining. Ghana’s petroleum revenue management laws require the government to report both revenue and expenditure and compel it to allocate a significant portion of oil revenues to specific programs and sectors.

To maximize revenue and broader benefits during the transition years, Ghana needs a new fiscal regime that specifically governs its transition minerals. A business-as-usual approach will hurt the country’s domestic revenue and slows plans for its own transition.

Regulations specific to transition minerals will offer a context-specific framework to guide and govern the sector as well as respond to ongoing global regulatory reforms on transition minerals.

Ghana can learn from other countries’ examples. In 2020, Canada and the United States finalized a Joint Action Plan on Critical Minerals Collaboration. The Canadian government subsequently published a list of 31 minerals identified as “critical.” In 2022, it released a policy statement on how the Investment in Canada Act will apply to investments in Canadian entities and assets in transition minerals sectors. Among others, acquisition of control in companies in this sector will now require ministerial-level approval

The U.S. passed the Energy Act 2020 to introduce reforms and increase investments in technologies to help the country’s energy transition. There are specific provisions for a national strategy on critical minerals production and the country’s independence in the production of such minerals.

In response to the 2022 Versailles Declaration, European Union President Ursula von der Leyen announced the Critical Raw Materials Act in March 2023 to address the EU’s dependency on imported critical raw materials by diversifying and securing a domestic and sustainable supply of critical raw materials. (Though the draft CRMA does not adequately protect against corruption.)

These exact objectives of these regulatory reforms may differ slightly from what Ghana may need. However, they all aim at maximizing states’ interests in these “critical minerals” in the context of the energy transition. Ghana can thus take a cue and act proactively.

Fiscal frameworks designed for Ghana’s transition

These examples indicate that the world is moving at a very fast pace on transition minerals access and control. Can Ghana afford to revert to its old mineral fiscal regimes in this highly competitive environment for transition minerals? To do so may lead to substantial revenue losses and would reduce the country’s status in the transition race to that of a mere producer of raw materials. (The existing regime has several provisions such as development agreements and exemptions that are not tailored to the transition minerals.) The current fiscal regime for mining provides several stability clauses, development agreements and other tax exemptions that erode the country’s domestic revenue. Ghana’s mining sector is prone to illicit outflows, and loses an estimated USD 2 billion annually through smuggling. The government can address these loopholes with targeted sets of regulations.

Ghana needs a transition minerals law to govern the contracting, extraction, processing, export and usage of revenues. The country will benefit from specific regulations to ensure that our transition minerals are refined domestically, and not exported in their raw states as has happened for over a century with Ghanaian gold, bauxite and other minerals. Adding value to these minerals will enhance Ghana’s export revenues to compensate for the expected decline in proceeds from the export of fossil fuels.

The regulation should also guarantee access to secure, affordable and sustainable transitional mineral supplies for the country’s own nuclear and other energy generation operations dependent on green technologies. Most importantly, the government must enforce the law when passed so that it does not suffer the fate of so many other laws that remain toothlessly unimplemented.

And the law should include specific provisions for investment in the sector, including foreign ownership and controls.

Without a new set of regulations that are fit for purpose, Ghana will soon find itself playing catch-up to the rest of the world amid the energy transition. Even with revenue from fossil fuels, Ghana continues to struggle with high unemployment, weak domestic revenue, negative trade balances and persistent balance of payment problems. Weakness in its governance of increasingly crucial transition minerals will only exacerbate these problems.

To conclude, having a new framework specifically for transition minerals will ensure fit-for-purpose governance structures that promote responsible access, increase investment and ensure Ghana’s share of the revenue needed for its own energy transition. To achieve a triple win for Ghana’s minerals, the approach must be different this time.

Governance of transition minerals is critical

Boom or Bust: Will Mineral-Rich Countries Benefit from the Energy Transition?

The energy transition is driving demand for minerals needed for low-carbon technologies, such as solar panels, wind turbines and electric vehicles. This demand could grow by up to 900 percent for some minerals over the next two decades, yet technological innovations also make these projections uncertain. According a new report from the Extractive Industries Transparency Initiative (EITI), produced by the University of Queensland, EITI implementing countries will likely play a substantial role in satisfying growing demand.

Government officials in many mineral-rich countries are excited about the mining sector’s economic promise. They are hoping for new investments that will bring in revenues, jobs and opportunities for local businesses.

But the prospects for converting natural resource wealth into sustainable development outcomes hinge on good governance (addressed in this new report from the Natural Resource Governance Institute [NRGI]). History points to the corruption and public finance risks that a mining boom can bring, including bribery in licensing, inadequate environmental and social assessments and lost revenues due to weak tax collection. In some cases, the mere anticipation of an uptick in investment could destabilize economies in mineral-rich countries.

Corruption in licensing and procurement

The business opportunities associated with a mining boom could be vulnerable to corruption. One key risk relates to the award of mining licenses. In many countries, authorities rush to approve new mines, with governments seeking to speed licensing processes. Peru, for example, has streamlined community consultations, and Brazil has introduced a policy to expedite approvals for mines of strategic importance. As flurries of applications stretch the capacities of government departments, companies may be increasingly tempted to offer bribes to speed up approvals, especially in a highly speculative context characterized by geopolitical competition between economic superpowers to secure transition mineral supply.

Officials may also feel pressure to cut corners and bypass due diligence checks, increasing the risk of politically connected (or/and unqualified) companies acquiring mining rights, or of weak or manipulated socio-environmental assessments. This can be particularly problematic since some transition minerals are located in unmined, environmentally fragile areas, in countries that are sensitive to environmental and social impacts. For example, mining projects in the “lithium triangle”—which comprises Argentina, Chile and Bolivia—could further strain the region’s limited water resources.

Similarly, the procurement of goods and services by mining companies can be vulnerable to corruption. Research by the OECD has found this to be a key risk area in the mining sector.

Transparency and multi-stakeholder dialogue can help to mitigate these risks. Governments should clearly justify any “fast-tracked” awards processes and commit sufficient time and resources to due diligence checks. Mining companies can support anti-corruption efforts through commitments to strong business integrity practices and due diligence processes across their business units. The EITI’s expectations for supporting companies, to which many of the world’s largest mining companies are committed, provides a starting point.

Uncertainty around public finances

Even if a country has abundant mineral reserves, weak governance and a lack of transparency can foil potential investment. For example, countries may struggle to attract high-quality, responsible mining companies in the absence of robust, publicly available geological data. Yet only four EITI implementing countries—Colombia, Indonesia, Kazakhstan and Mongolia—have adopted the CRIRSCO good practice guidance for public reporting of exploration results, mineral resources and mineral reserves.

Even if the sector grows, producing countries and investors will not be in a position to take fully informed decisions because of the uncertainty around economic prospects. Price volatility may lead to unpredictable revenue flows and macroeconomic planning challenges. Governments may collect less revenue than officials anticipate as a result of opaque tax structuring by companies operating across transition mineral value chains. In 2018, Chile had to create a committee to supervise lithium contracts after allegations of transfer pricing abuse.

Governments of resource-rich countries should promote transparency and accountability of the sector to mitigate these risks and realize their mining potential. They should publish more detailed information on the reserves and economic potential of transition minerals; strengthen oversight of companies’ revenue flows and financial relationships; and promote policies that support long-term economic planning and transparent decision-making.

Opacity in commodity trading and state participation

As resource-rich countries seek to take advantage of global competition for transition minerals, some are expanding the role of state-owned enterprises (SOEs) in the mining sector. For example, in the Democratic Republic of the Congo, the state recently established the Entreprise Générale du Cobalt (EGC) to manage all artisanally mined cobalt. In Indonesia, SOEs manage trade of tin, nickel, bauxite and other minerals.

Lack of transparency of revenue flows between governments and SOEs is a known risk, especially where SOEs are involved in the sale of the state’s share of production. While the oil and gas sector has been particularly vulnerable to corruption in commodity trading, the mining sector could face similar risks as governments increasingly involve SOEs to seize opportunities coming from growing demand for transition minerals.

For countries that foresee a strong role for SOEs, it is important that authorities identify associated governance and corruption risks and institute measures for mitigation, both for partners of SOEs and the SOEs themselves. Like companies in the private sector, there is no reason why SOEs cannot commit to high integrity standards across their business units and establish processes for risk assessments and due diligence checks, including when dealing with commodity traders.

Based on past experiences, only a well-managed mining sector will contribute to sustainable development in mineral-rich countries. Without high governance safeguards and real anti-corruption efforts, countries will lose out on potential revenues, deter investment, miss the opportunity to diversify their economies and increase risks of negative socio-environmental impacts. The result will be a mining boom that fails to deliver on its economic promises and an energy transition that may not advance global decarbonization at the speed needed – or advance it at the expense of the citizens of mineral-rich countries.

This post appears also on the EITI website.

Uganda’s Local Governments Need Clarity on Oil Revenue Sharing

Driving from Hoima to the breathtaking banks of Lake Albert, where Uganda’s long-awaited 1.4 billion barrel oil project is located, it is clear that the government has been preparing for production for years. New roads and bridges criss-cross the region. However, one area in which the government is unprepared is the sharing of oil royalties with the region’s districts.

Section 75 of the Public Financial Management Act 2015 (PFMA) provides for the sharing of royalty revenues with local governments, and cultural or traditional institutions named in the government gazette. But the law is vague about the precise sharing mechanism. The challenges that this is causing for districts in the oil-rich region were apparent in a workshop that NRGI held with civil society organizations there earlier this month: scarcity of details has frustrated local officials’ planning and their management of public expectations. With production likely to start in just three years, the national government is running out of time to address these challenges.

Providing clarity to subnational authorities is all the more important given the uncertainty that the energy transition has created around estimates of the total royalties that the Ugandan government will receive. Local governments and cultural and traditional institutions don’t have a sense of how much funding they can anticipate. The speed of the world’s shift away from oil will impact the price that the Lake Albert oil commands, as well as the potential for subsequent oil projects in the country.

To bring some of that much needed clarity, we developed a simple model which helps subnational entities assess how much revenue they might receive. The chart below shows the possible local government share from the Lake Albert project in three global demand scenarios, based on our modeling. The Announced Pledges Scenario (APS) from the International Energy Agency (IEA) assumes that countries implement the climate commitments that they have made to date. The reference scenario of the Organization of the Petroleum Exporting Countries (OPEC) envisages a slower transition, while the IEA’s Net Zero (NZE) scenario assumes that the world manages to achieve net zero emissions by 2050 and therefore sets out a much faster transition. (All of these scenarios have been updated by Rystad Energy to reflect developments since they were generated and converted to implied prices.)

Local government share of royalty across possible price scenarios

Local government revenues differ significantly between these three scenarios. In the OPEC scenario, Uganda’s local governments could receive around $20 million a year on average. As our model shows, this amount is more than double the revenues that districts in the region were expected to raise through normal, non-oil means in 2021/22 (using the initial list of districts that would receive a share). In the NZE scenario, the local government share of oil revenues would be much less, possibly around $0.6 million. Though even this smaller amount could be significant for some individual districts if managed carefully.

How revenues will be shared between individual subnational entities is currently unclear, however. As our model highlights, the gaps in detail about the sharing mechanism make this assessment impossible.

Uganda’s Ministry of Energy and Mineral Development and Ministry of Finance, Planning and Economic Development can clarify the situation by answering four key questions:

Which districts and cultural or traditional institutions will receive a royalty share?

The law states that six percent of total royalty revenues will be shared among the local governments “located within the petroleum exploration and production areas.” How these areas will be defined is unclear. An early version of the public financial management bill specifying districts that will receive a share (including some districts which are not home to any granted petroleum licenses) has confused this issue further. This list was retracted in 2015, but another list is yet to be published by the Ministry of Energy and Mineral Development. One percentage point of the royalty due to the central government will also be shared with “gazetted cultural or traditional institutions.” However, which institutions will be gazetted is similarly unclear.

What criteria will be used to create the sharing formula, and how are they defined and weighted?

Fifty percent of the local government share will be divided among local governments involved in production based on their production level or “impact,” according to section 75 of the PFMA. The other 50 percent will be shared among all local governments based on “population size, geographical area and terrain.” However, the formulas in the law’s schedule 6 only include production level and population size. Clarity is therefore needed from the government on whether the criteria in section 75 or the criteria in schedule 6 will be used, how each criterion is defined and, if the formulas are to contain more than one criterion, how the different criteria will be weighted. For example, the first fifty percent will likely be divided between five districts if production level is the only criterion, but it could be divided between a lot more districts if impact is also included depending on how it is defined. For example, if all the districts through which the East Africa Crude Oil Pipeline runs are seen as impacted.

What share will cultural or traditional institutions receive?

The amount that “one percentage point of the royalty due to the central government” entails isn’t clearly defined. For example, if the total royalty revenue is USD 100 million in a given year, the central government will initially receive $94 million (with the remaining $6 million being shared among local governments). Whether cultural or traditional institutions will receive $1 million (representing 1 percent of total royalty revenue) or $0.94 million (representing 1 percent of the royalty revenue received by central government) is not clear.

What are the rules governing how subnational entities manage revenues?

The PFMA earmarks local governments’ royalty revenues for “development purposes.” However, there is a risk that local governments could apply a broad definition to development purposes and, as a result, won’t spend petroleum revenues as intended. There is no instruction in the PFMA for how cultural and traditional institutions should spend their share of royalty revenues nor for what happens to royalty revenues that are unspent by recipient entities. Section 17 prevents local governments from retaining a budget allocation after the end of a given financial year. However, providing access to leftover oil funds in subsequent years will be important so that local governments don’t spend money ineffectively to avoid losing it. This will also prevent them from smoothing spending as royalty revenues fluctuate with production and prices.

The challenge of establishing an extractives revenue sharing mechanism that benefits communities is not unique to Uganda. NRGI’s work in countries such as Indonesia highlights the difficulty in ensuring revenues are shared based on a clear and predictable formula that is broadly seen as fair. Such complexities have led to delayed implementation in several countries, such as Guinea, reinforcing the need for the Ugandan government to start focusing on this issue now.

And establishing the mechanism is only the first step. As the past experience of Peru highlights, even if Uganda strengthens its rules for managing subnational revenues, increasing the capacity of local governments to address the unique challenges of resource revenues will be critical. Similarly, Colombia provides lessons on the importance of developing transparent processes for both the distribution and use of funds.

Uganda therefore has significant work to do to ensure that revenue-sharing will benefit communities in the oil-producing region. But until the central government addresses the four gaps outlined above and provides clarity on the revenue sharing mechanism, local governments and communities will be making plans based on guesswork.

Colombia: Inclusion and Upgraded Governance Are the Keys to Petro’s Energy Transition Ambition

This is a shortened translation of a longer Spanish-language post.

On 7 August, Colombia turned a new page in its history. For the first time South America’s second-most populous country will be governed by a left-wing president and an Afro-Colombian vice-president who is a seasoned leader of social movements. More than 11 million citizens (50.44 percent of those voting) gave President Gustavo Petro and Vice President Francia Márquez Mina their mandate.

Petro boldly stated in his inaugural address that “we are willing to move to an economy without coal and without oil.” But how can the government and Colombians translate these green ambitions into concrete results?

In addition to addressing fiscal and energy supply challenges, the government must commit to good governance of the energy transition away from fossil fuels. The transition must include diverse voices and be transparent. Authorities must define clear policy frameworks for managing the progressive decline in production of fossil fuels, the need for economic diversification and the new governance challenges of renewable energies and transition minerals.

Petro's energy transition agenda

President Petro’s proposal to limit oil extraction has positioned him as a changemaker in the global energy transition. During his campaign, he invited other leaders in the region to form an “anti-oil bloc” to move economies away from fossil fuels and create a Latin American front to fight climate change. A few days ago, he received a letter signed by more than 80 parliamentarians from 30 countries that are part of the movement called “Call of Parliamentarians for a Future Free of Fossil Fuels” expressing their support to his proposal. Indeed, as an oil-producing and oil-dependent country, Colombia could become a laboratory for the innovation of transition policies, with much to contribute to other producing countries and global efforts to mitigate warming.

In line with Colombia’s updated commitments to the Paris Agreement—51 percent reduction in greenhouse gas emissions by 2030 and zero net emissions by 2050—during the campaign, Petro argued that Colombia should cease licensing for new hydrocarbon exploration and for large-scale open pit mines; ban the exploration and exploitation of offshore and non-conventional hydrocarbon deposits; and stop fracking pilot projects.

Petro also proposed promoting non-conventional renewable energy sources and earmarking the exploitation of fossil fuel reserves for domestic consumption, given their low levels (7.6 years’ worth of oil and 8 years’ worth of gas). In addition, he pointed out that Ecopetrol (which is majority state-owned), should play a fundamental role in the transition by redirecting part of its exploration budget toward a new energy transition fund.

After winning the election, Petro moderated some of these proposals. In his inaugural speech, he pointed out that although his commitment to decarbonization remains, Colombia is not a major contributor to global emissions. He also placed a greater focus on the role of international cooperation. The newly appointed finance minister, José Antonio Ocampo, has indicated that gas exploration will probably continue and that oil exports should continue in the short term. In a recent interview, the new mining minister, Irene Vélez, also commented that this process would take more than a decade and that the government would discuss the extraction of minerals necessary for technologies needed for the energy transition.

Top-down decision-making, general exclusion of affected communities and negative project impacts have generated a high level of socio-environmental conflict in the territories where extraction takes place.

Former president Iván Duque took important steps toward the energy transition by promoting investments in renewable energies, some green hydrogen pilot projects and transition minerals. But his administration also prioritized the expansion of fossil fuel extraction. He supported the coal industry to increase its competitiveness in the Asian market, promoted offshore hydrocarbon exploration projects, and encouraged pilot fracking projects to increase gas supply. Top-down decision-making, general exclusion of affected communities and negative project impacts have generated a high level of socio-environmental conflict in the territories where extraction takes place. This perpetuated a trend that began in the early 2000s.

Four challenges to Colombia’s energy transition

If Colombia does not initiate a broad discussion and take steps toward a just transition, in a few years it could end up with stranded assets and investments with low economic, social and environmental returns that could increase inequality. However, President Petro will have to lead this process in a scenario of great economic uncertainty linked to inflation and the risks of a global recession—in addition to the difficult fiscal situation resulting from the coronavirus pandemic.

Fiscal policy

In the past, as much as 25 percent of government income has come from hydrocarbons. Managing the progressive decline in hydrocarbon production means replacing taxes on oil and gas with new sources of revenue.

The new government has proposed imminent tax reform with the aim of raising COP 25 trillion (approximately USD 5.5 billion). The success of this proposal will be a key indicator of how and when the government might cover the gap that would be left by an eventual reduction in oil and gas taxes and royalties.

The redefinition of Ecopetrol’s role will be of great significance since its profits are an important contributor to the state budget. It is an efficient company that has achieved good financial results in recent years despite the pandemic and its profits will help to cover this year’s fiscal deficit.

The energy crunch resulting from the war in Ukraine will likely sustain the recent increase in hydrocarbon prices for some time to come.

Government officials will also need to decide whether or not to maintain the commitment to the promotion of the exploitation of minerals, which have contributed less to government coffers than oil and gas. The new government has announced a mining moratorium during its first 100 days so that officials can review compliance with regulations, but in other declarations has opened the door to further exploitation of transition minerals such as nickel and copper. Should authorities further pursue those commodities, they should also develop a modern taxation framework as well as enforceable socio-environmental standards adapted to the new importance of these metals.

Finally, the pace of the global energy transition is a key consideration for Colombia’s revenues in the short term. It is likely that in the long-term oil and coal prices will decrease. But the energy crunch resulting from the war in Ukraine will likely sustain the recent increase in hydrocarbon prices for some time to come. Petro has shown a willingness to take advantage of the boom in the short term.

Trade deficit

Another economic challenge to consider relates to the current account deficit. In 2021, the oil industry represented 33 percent of the total value of Colombian exports. Along with coal and other minerals, oil and its derivatives account for about 56 percent of the total value of the country’s foreign sales and generate annual foreign exchange earnings of about USD 20 billion. Likewise, oil license bid rounds and mining investments are a main source of foreign direct investment (USD 7.6 billion in 2020). In this context, the new minister of finance has suggested the need to continue exporting oil to avoid a problem in the balance of payments.

Energy supply

In 2018, 70 percent of Colombia’s energy supply derived from fossil fuels (40 percent on oil and derivatives, 21 percent on natural gas and 9 percent on coal.) Liquid fuels derived from oil are especially important in the transport sector (96 percent of consumption) while gas is key for industry and households. In this context, the government must define a path for its progressive reduction at the same time as it ensures energy access for the most vulnerable communities. Renewables energies will play a key role.

Clean energy governance

In order to multiply investments in renewable energy, the government should establish clearer governance frameworks. The development of clean energy projects has generated strong criticism and opposition from local communities due to the absence of free, prior and informed consultation, environmental and social impacts, and a lack of understanding of the relationship between communities and their lands. This is especially relevant in La Guajira, a multicultural and multilingual department of Colombia with a 42 percent indigenous population, high levels of poverty and limited access to electricity, but with enormous potential for wind and solar energy (wind speeds exceed 9.8 meters per second, twice the world average, and solar radiation is between 6 and 7 kilowatt hours per square meter per day, 60 percent higher than the global average). It is essential that the government, elected with the support of ethnic minorities, resolves these tensions and ensures that local populations receive the benefits of the transition.

The way forward

In general, the new government has the challenge of building adequate governance for the transition, keeping in tune with social expectations, while meeting the needs of an economy recovering from the pandemic. Implementing policies to move away from fossil fuels will be complex from a political and economic point of view, so it is very important to guarantee a democratic process and avoid the influence of undue interests in the process.

The eyes of the world are on how Colombia, a country dependent on oil production, can make its own just energy transition.

Among other elements, officials planning for the transition should:

- disclose the possible impacts of the different transition scenarios and disseminate this information to different stakeholders.

- ensure broad and territorial participation in defining and implementing the transition, including the most vulnerable groups.

- articulate clear measures for the diversification of the economy and compensation that will allow those most affected by the transition to benefit.

Robust governance will also require a high degree of interinstitutional coordination, especially between public institutions, including at the local level, to avoid contradictory messages about the transition process and the future of extractive industries. The energy transition requires policies at all these levels and necessitates an interdisciplinary perspective. It may also require additional regulatory frameworks in new areas such as transition minerals or renewable energies as officials and citizens come to better understand the conditions of these markets and global trends, as well as the implications for communities.

The eyes of the world are on how Colombia, a country dependent on oil production, can make its own just energy transition. There is a huge potential to generate lessons useful to other countries. The challenges are vast, both fiscally and in terms of energy access. But the Petro administration can meet these and other challenges by establishing adequate governance of the transition. For this, Petro will need to cultivate a broad national consensus that includes the territories and a diversity of voices. The support of allies at the international level will also be essential.

The G7 Missed a Crucial Ingredient for a Green and Equitable Future. Here’s a Way Forward.

Last weekend leaders of the G7 group of wealthy countries recommitted to the value of democratic, open societies and declared lofty ambitions around the pandemic response, economic recovery, climate change and global infrastructure. But they left out a crucial element. Improved governance in resource-rich countries is essential for the billion people who live in poverty in countries abundant in oil, gas and minerals. Without it, they will be excluded from the “clean, green growth” needed for an effective global energy transition. Fortunately the major gatherings in the months ahead—notably the G7 interior ministers meeting in September and the COP26 climate summit in November—offer an opportunity for G7 governments to address the gap in their plans.

Here are five ways they can correct their course:

Wind down fossil fuel production and support low-income producer countries on governance fundamentals needed for the transition to clean energy

The G7 “advanced economies” have yet to fulfil their pledge to mobilize $100 billion in public or private funding to support energy transition in developing countries. Low-income resource-rich countries need support to transition to a future in which fossil fuel extraction delivers dramatically less income. At the same time, enabling them to decarbonize and diversify into renewables will require a major shift in incentives. G7 governments should:

- Promote a core set of government and company disclosure requirements on fossil fuel projects in all countries; this will enable the public to assess every project’s viability under different climate scenarios.

- Support accountability and economic planning capacity in low-income countries, to help align political incentives and capabilities around a sustainable path forward. G7 countries must fund the identification of options for lower-income countries that are more attractive than fossil fuel extraction.

- Lead by example and take more decisive action to wind down their own countries’ production of oil, gas and coal. It is unrealistic, and unfair, for wealthy countries to expect low-income countries to abandon the sector when G7 countries continue to license new petroleum fields.

Enact and support global standards on critical minerals governance

The G7 meeting and communiqué rightly touched upon the importance of resilience in the global supply chain of critical minerals from the perspective of economic recovery and jobs in their own countries, and called for sharing of best practice to address threats to supply. However, addressing governance and corruption risks in producing countries were missing from the G7 conclusions. Failing to address these risks will impact reliability of supplies and thereby threaten the clean energy transition which relies on increased use of minerals such as cobalt and lithium; it will also diminish the potential for citizens of producer countries to benefit from the extraction of these minerals. G7 governments should:

- Promote robust governance standards in mineral supply chain initiatives.

- Prioritize transparency, accountability, anticorruption and support to civil society in their assistance to low-income critical mineral producer countries.

Deploy the new infrastructure initiative with an emphasis on financial support, accountability and debt transparency

Last weekend the G7 announced a new approach to financing the significant infrastructure needs of low- and middle-income countries. The aim is to enable these countries to build back better post-pandemic, with a focus on quality infrastructure supporting “clean and green growth” based on the principles of transparency, sustainability and collaboration. (In recent decades, many resource-rich countries have financed infrastructure upgrades with opaque resource-backed loans, often from China.)

The initiative has been cast in the media, and will likely be viewed from low-income countries, as an attempt to compete with China, given the important role that the country has played in financing infrastructure in much of the world. Developing countries will likely view this increased interest and competition around infrastructure as positive. However, no announcements of specific financial support accompanied the G7’s plan.

In order for their new infrastructure initiative to succeed, the G7 governments should:

- Raise the bar on sovereign debt transparency, so that citizens can assess the impact of different financing options, including on resource-backed loans. Publication of key loan terms and loan agreements is essential. Greater transparency in direct G7 country lending will be important, as will a broader G7 push for transparency from private creditors. (In resource-producing countries, loans from commodity trading firms are often even more opaque than those from Chinese lenders and have destabilized whole economies.)

- Support borrower countries in adopting transparent debt approval and management processes.

- Follow through on the commitment to consult openly and collaborate with developing country governments, including as part of the new proposal development taskforce.

- Commit significant funding in the near term to get the initiative off the ground.

Include the concerns of resource-rich developing countries in global tax reforms

Tax avoidance and evasion are longstanding challenges for resource-producing countries. The G7 acknowledged the need to end the “40-year race to the bottom” on international tax—a welcome step. However, the G7 commitment doesn’t serve resource-rich developing countries. The proposed global minimum corporate tax rate of 15 percent is likely too low to prevent profit shifting in the extractive sector as producer country tax rates for the sector are often significantly higher. Developing countries are also unlikely to acquire much additional revenue from applying the 15 percent rate to profits booked in low-tax jurisdictions as the G7 is silent on who collects those, suggesting that most will go to multinational companies’ headquarters jurisdictions, as per an OECD proposal. The emphasis on allocating taxation rights to “market countries” (i.e., where goods or services are consumed) rather than producer countries also means that resource-rich countries may even end up with less revenue than they collect now unless the sector is exempted (as was previously agreed in the OECD context).

G7 governments should integrate the concerns of resource-rich developing countries into the OECD/G20 Inclusive Framework when these tax reforms are refined later this year.

Tackle fossil fuel sector corruption, state capture and kleptocracy—with a climate lens

Corruption is an overlooked threat to a successful energy transition. In fossil fuel-producing countries, corruption and narrow political agendas can mean that leaders invest more in oil, gas and coal projects; lavish these industries with subsidies; and block progress on greener energy—even when doing so runs counter to climate goals and citizens’ economic and environmental interests. Elites behind fossil fuel company lobbying and campaign donations can (often legally) influence or even direct energy and climate policy.

Half of the world’s oil is produced by 13 authoritarian countries, including several run by kleptocratic regimes with few incentives to move away from fossil fuel production. Meanwhile, as we have discussed above, the boom in demand for minerals required for clean energy could also trigger surges in corruption like those associated with past oil booms. G7 governments, including the G7 interior ministers meeting in September with their focus on strengthening international action against corruption and kleptocracies, should:

- Explicitly acknowledge the extractive sector as high-risk and recognize that strong action on anticorruption in fossil fuels and critical minerals is also good climate policy.

- Build on the commitment to greater beneficial ownership disclosure by requiring greater transparency in areas where the fossil fuel industry and governments interact, such as lobbying and government contracting, commodity trading, subsidy payments and national oil company finance.

- Seek fresh responses and modes of cooperation, including punishment for Western enablers who help kleptocrats to profit and thrive.

Leaders of G7 countries must turn their rhetoric into reality in the months ahead; they can do so by urgently prioritizing the governance of fossil fuels and critical minerals in producer countries, and making concrete commitments as described here. The “green revolution” cannot otherwise succeed.

This post was written by a group of NRGI experts.

Three Proposals for Mineral-Dependent Countries During the Coronavirus Pandemic

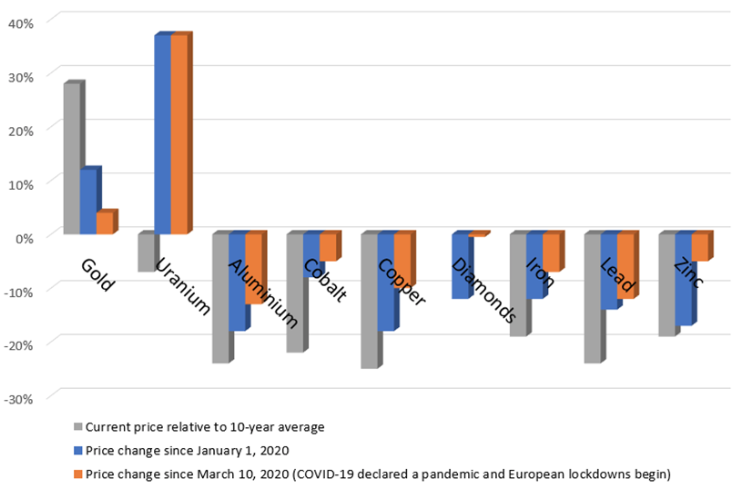

Coronavirus containment measures have hit economies hard—and with them, government revenues. Most natural resource-dependent countries are experiencing a double shock as their main source of foreign currency has crashed along with fiscal revenues. The situation is most severe in oil-dependent countries; oil prices have declined by more than 60 percent on average since the start of the year, and occasionally dropped below $0 a barrel. Mineral-dependent countries have been affected too, but in more surprising ways.

Gold and uranium prices have climbed, driven by a combination of safe-haven buying and production cuts. As one senior mining official from a gold-producing country said on a webinar recently, “[The companies] are making money!” Governments dependent on these minerals, such as in Burkina Faso, Guyana, Kyrgyzstan, Mali, Niger and Suriname, will be able to offset some of the revenue lost in other sectors through increased mining receipts. How much of a buffer gold or uranium revenues will provide depends largely on these countries’ fiscal terms and how well they negotiated their mining contracts to integrate a progressive tax regime to take advantage of more profitable periods.

However, prices of the other most widely traded minerals have collapsed by 8 to 18 percent since the start of the year. While there was a slight recovery in April, in general prices remain low by historical standards but unpredictable.

Selected mineral price changes since coronavirus outbreak (spot markets as of late April)

Sources: London Metals Exchange; Ziminsky Global Rough Diamond Price Index; Trading Economics

Sources: London Metals Exchange; Ziminsky Global Rough Diamond Price Index; Trading Economics

Mine shutdowns are, in some cases, doing worse damage to public finances than low prices. Production is being cut as mines suspend operations or reduce output to prevent spread of the virus, even where prices are high enough keep a mine profitable. For instance, Peru’s enormous Antamina copper and zinc mine is being suspended to contain the outbreak. Mexico has suspended production at all mines. Malaysia and Mozambique suspended their bauxite mines. South Africa has reduced mining production by 50 percent following a full shutdown. Further disruptions, whether to prevent the spread of the virus or in response to infections at mine sites, are likely, despite some governments’ efforts to keep production going by declaring mining an essential service.

Shutdowns and weak prices are hitting certain countries harder than others. In 2016, 27 percent of Guinea’s fiscal revenues, 26 percent of Zambia’s and 24 percent of the Democratic Republic of the Congo’s (DRC) were paid by mining companies. Even these high numbers underestimate the governments’ dependence on the mining sector, as they do not include income taxes from mine workers and taxes from mine suppliers. The longer the containment measures persist, pushing down demand and increasing stockpiles, the greater the pain for mineral producers will be.

Still, the main worry for many mineral-dependent countries is not just the decline in fiscal revenues. Rather, it is that many will face balance-of-payments crises, meaning they will not have enough foreign currency to pay for imports or service external debts. Mineral exports are the primary source of foreign currency for more than 20 countries, including Eritrea, Mongolia and Tajikistan.

In a handful of countries with small foreign reserve buffers and limited access to foreign capital, sovereign debt crises may coincide with balance-of-payments crises. As the export dependence, foreign reserve and credit default swap (CDS) spread (an indicator default probability) figures in the table below indicate, several African countries, including DRC, Guinea, Mauritania, Sierra Leone and Zambia, are at high risk of these dual crises.

Mineral-dependent countries’ risk of sovereign debt and balance-of-payments crises

| Country | Main mineral exports | Mineral exports as a percentage of total exports (2017 or most recent) | Risk of debt distress (based on CDS spreads, IMF DSAs and govt reports) | CDS spread on sovereign debt (as of April 1, 2020) | Reserves by months of imports (2018 or most recent) |

|---|---|---|---|---|---|

| Australia | Iron, coal, gold | 62% | Low | 0.0% | 2 |

| Bolivia | Zinc, gold, lead | 49% | Low | 6.7% | 8 |

| Botswana | Diamonds | 91% | Low | 1.3% | 9 |

| Chile | Copper | 56% | Low | 1.0% | 4 |

| Namibia | Diamonds, copper | 61% | Low | 4.5% | 4 |

| Peru | Copper, gold, zinc | 63% | Low | 1.8% | 11 |

| South Africa | Gold, diamonds, platinum, iron | 60% | Low | 3.7% | 5 |

| Tanzania | Gold | 43% | Low | 6.7% | 6 |

| Burkina Faso | Gold | 85% | Moderate | 8.2% | - |

| Ghana | Gold | 53% | Moderate | 9.6% | 3 |

| Guyana | Gold, aluminum | 51% | Moderate | 9.7% | 2 |

| Kyrgyzstan | Gold | 57% | Moderate | 8.2% | 4 |

| Mali | Gold | 63% | Moderate | 9.7% | - |

| Mongolia | Copper, coal | 91% | Moderate | 9.7% | 4 |

| Niger | Uranium | 60% | Moderate | 9.7% | - |

| Papua New Guinea | Gold, copper | 45% | Moderate | 8.2% | 4 |

| Suriname | Gold | 80% | Moderate | 8.2% | 3 |

| Tajikistan | Aluminum, gold, zinc, lead | 78% | Moderate | 9.7% | 4 |

| Congo, DR of | Cobalt, copper | 90% | High | 11.1% | 0 |

| Eritrea | Zinc, copper | 97% | High | n/a | 1 |

| Guinea | Aluminum, gold | 81% | High | 14.8% | 3 |

| Mauritania | Iron, gold, copper | 53% | High | n/a | 3 |

| Mozambique | Coal, aluminum | 69% | High | 13.4% | 4 |

| Nauru | Phosphates | 74% | High | n/a | 4 |

| Sierra Leone | Iron, titanium, diamonds | 67% | High | 14.8% | 3 |

| Zambia | Copper | 84% | High | 15.00% | 2 |

What can officials do, bearing in mind that each country faces its own challenges and no single policy would be applicable in every context?

1. Support mine workers and foreign exchange generation rather than shareholders

The mining sector produces fewer jobs per dollar of revenue generated and has smaller economic spillovers than almost any sector. But mining is a major employer in some countries and localities. In many countries, it is also an important generator of much-needed foreign currency.

Authorities should design financial relief measures for mines to meet specific policy goals, and only apply them to mining projects that are suffering from historically low commodity prices. If the goal is to keep workers employed, it is better for governments to pay a portion of workers’ salaries as long as they are kept on the payroll or defer payroll taxes, rather than bail out companies and their shareholders. If the goal is to maintain operations, governments can provide logistical support to mines, for instance through virus testing and keeping key trade routes open.

2. Resist impulsive tax relief and subsidy measures

Mineral prices are likely to trend toward their medium-term averages, though it is difficult to know when, given global uncertainty around demand and coronavirus containment. In the meantime, mining companies, employees and business associations are pressuring officials for tax relief and subsidies as compensation for shutdowns, sometimes successfully.

There are serious risks associated with renegotiating mining contracts or changing tax regimes in a manner that fails to capture future profit increases. Past experience shows that governments often fail to cancel tax relief after prices have risen again. Further, asset owners are in weak negotiating positions when prices are low.

Introducing sliding royalties might be one approach to providing temporary relief while automatically responding to a price rise. Sliding royalty rates automatically fall when prices fall, providing some relief in the current context, and rise when prices recover.

3. Distinguish between public sector liquidity and solvency crises

In some mineral-dependent countries, the drop in fiscal revenues will generate significant burdens on public finances. Many governments will need to further indebt themselves to overcome a temporary shock to fiscal revenues. However, in a handful of countries, the twin shocks are likely to push them over the edge into insolvency.

Countries in liquidity crises must find sources of financing to withstand the next couple of years. While the G20 have offered support, more will be needed. Temporary debt relief is part of the solution. Additional borrowing from institutional investors and the central bank may also be necessary. Debt monetization is an option worth considering during a contractionary spiral, especially in countries with shallow financial sectors and limited access to international capital, but with adequate foreign reserves to prevent a major depreciation. Where governments are insolvent, debts must be restructured immediately to create the fiscal space to respond to the coronavirus crisis and set themselves up for growth once the crisis is over.

Coronavirus, the Oil Crash and Economies: How Can Governments of Oil-Dependent Countries Respond?

Français »

The battle against the coronavirus is above all a public health crisis. Needless to say, the response to the crisis is having enormous economic repercussions. Some countries have imposed sweeping shutdown and isolation measures to contain the spread. As a result, businesses are closing and unemployment is soaring.

Countries that are net exporters of oil and gas will perhaps experience the biggest shock. As of early April, Brent crude was trading at USD 25 per barrel and forecast to decline, a result of plummeting demand, a growth in supply and a lack of storage capacity. This represents the biggest single negative oil price shock in modern history.

Central banks have been the first public authorities to respond to the crisis in many oil-dependent countries. For example:

- The Emirati and Saudi Arabian central banks announced support for small and medium-sized enterprises (SMEs) totaling USD 40 billion.

- The Bank of Canada announced about USD 30 billion in lines of credit.

- Oman’s government announced USD 20 billion in support for its banks.

- The Central Bank of Nigeria created a USD 136 million targeted credit facility.

- The Central Bank of Iran ordered commercial banks to extend low interest loans to ten types of businesses most affected by the coronavirus outbreak, including restaurants, textile companies and dried nut shops.

But central banks can only provide liquidity; they cannot prevent insolvencies. In response, several oil-dependent governments have promised to enact fiscal stimulus packages. In addition to a discount on electricity bills and free internet, Malaysia has focused on cash transfers, including a one-off USD 144 for tourist guides, a monthly USD 150 for medical personnel, and money for specific groups such as low-income households, civil servants and students. Iran is providing cash payments to the poorest households, while Kazakhstan is providing free groceries to the disabled and unemployed. Canada’s oil-rich province of Alberta is allowing people to defer electricity and gas payments. Russia reduced social insurance contributions for SMEs, increased unemployment benefits and sick leave, and increased monthly child support payments by USD 63 per child under 3 years of age. Qatar announced a USD 20.6 billion package, including food and medical goods customs exemptions and utilities bill exemptions for SMEs. Governments are set to announce more support measures soon.

What will these measures achieve? Will stimulus boost economic production, keeping people in jobs, especially where social safety nets are weak? And how will the impact differ in oil-dependent states versus more diversified economies?

First, national experiences will depend on whether governments have prepared for a crisis. Kazakhstan, Kuwait, Malaysia, Norway, UAE, Russia, Saudi Arabia and Trinidad and Tobago have enough fiscal space to maintain public spending well into 2021 despite a collapse in government revenue, as suggested by CDS spreads on their sovereign debt, an indicator of default probability, as well as net debt figures. Each has significant savings in sovereign wealth funds or relatively low public debt levels. Moreover, with the exception of Malaysia and Trinidad and Tobago, each produces oil relatively cheaply, meaning their oil sectors are likely to generate significant revenue for their governments once the worst of the crisis is over.

Other governments of oil-producing countries had weaker public sector balance sheets heading into the crisis. Ecuador may default on its debt within the month. Nigeria’s sovereign debt rating was downgraded. Venezuela ran out of fiscal space to provide stimulus years ago. And Iraq does not have the administrative capacity to address either the economic crisis or health emergency. None of these countries is likely to be able to effectively mitigate the impact of the crash through more borrowing or drawing down on savings; the same is true for many other low-income oil producers.

Second, for many oil-dependent countries, the sharp drop in oil prices may lead to a disproportionately large fall in oil revenue. If prices remain low, some companies operating in countries where it’s relatively expensive to produce oil (such as Angola, Brazil, Canada, Malaysia, Trinidad and Tobago, the United States and Venezuela), could go bankrupt, leading to sustained lower output. In some places, oil production may never again reach pre-crisis levels due to technological “shut-ins.” Officials in many high-cost producer countries should expect a long-term decline in GDP rather than a temporary shock and therefore should not expect to “spend their way” out of the slump.

Third, governments of oil-dependent countries aiming to stimulate their economies through fiscal transfers to businesses face limited choices of where to allocate money. Many countries have only small and nascent productive sectors outside the oil industry. Economies in places like Algeria, Angola, Azerbaijan, Libya, Saudi Arabia, Timor-Leste and Trinidad and Tobago are not diversified, meaning there are fewer businesses that, with financial support, could quickly generate jobs and keep the economy churning. Even where there are businesses to support, governments cannot support many of them, since increased economic activity in some industries and much of the service sector risks spreading the virus. Officials in oil-dependent countries may therefore need to direct stimulus packages toward vulnerable groups, such as the poor or jobless, rather than businesses.

*Sovereign wealth fund asset values and GDP have declined since the crisis began

Sources: SWF annual reports or equivalent, IMF WEO, Damodaran (2020), WB WDI and Rystad Ucube.

Each country faces its own challenges, as illustrated in the table; no single policy would be applicable in every context. That said, officials in net hydrocarbon exporting countries could consider several general principles as they formulate their policy responses to the crisis:

1. Consider the role of sovereign wealth funds and borrowing

As mentioned, some governments entered the crisis with significant fiscal space, thanks to large sovereign wealth fund savings or low debt levels. Fiscal responsibility during boom years is designed to provide the space to draw down on savings or borrow during periods of crisis, such as now. Short- to medium-term borrowing may make sense now, with historically low interest rates available for those countries with access to credit. Governments may be wise to rely on models to determine how much fiscal space to use.

On the other hand, several oil-dependent countries have entered the crisis following a borrowing binge. Angola, Cameroon, Chad, Colombia, Republic of Congo, Ecuador, Equatorial Guinea, Gabon and Mexico were among those who had approached the International Monetary Fund before the crisis for program financing or a line of credit, meaning they already had difficulties financing themselves at higher oil prices. In recent weeks, Ecuador, Iran and Nigeria were among the 85 countries that approached the IMF for emergency assistance. Countries without fiscal space will at the minimum need to negotiate a moratorium on servicing external public debt, including repayments of oil-backed loans to oil traders and Chinese policy banks, and seek emergency support from multilateral and bilateral donors.

2. Resist the temptation to provide stimulus to the oil industry, whether through subsidies or tax cuts

There is a great deal of uncertainty around medium-term oil prices; some analysts suggest that they will not rebound for some time, while others say that the industry will contract quickly, leading to supply challenges and a swift price rebound next year. At the same time, public and private oil companies in several countries have been requesting large bailouts or tax relief. Government officials must consider the risks of “throwing good money after bad,” especially given the enduring climate challenge and the need to shift to renewable energies. Governments ought to resist hasty demands and properly evaluate (and model) the viability of projects at lower prices. If an oil company is facing insolvency, alternatives to a bailout can include seeking new investors or returning licenses to the state.

3. Devalue currencies slowly (in some countries)

Lower oil prices means far less foreign currency entering government coffers. This is already putting pressure on currencies. The implication is that countries like Ecuador, Iraq, Saudi Arabia and Timor-Leste and the CEMAC monetary union (including Chad, Gabon and Republic of Congo), which have dollarized or pegged their currencies to the U.S. dollar or the euro, will need to draw down on their foreign reserves or sovereign wealth fund savings or borrow foreign currency to maintain their pegs. Some countries, especially in the Persian Gulf, have the foreign savings to withstand years of low oil prices. But officials in others may need to choose whether to maintain their pegs, essentially subsidizing imports using their national savings, or devalue their currencies, leading to higher prices for imported goods, especially basic goods such as food, processed fuel and medication. As some countries run low on foreign currency, they may have to either seek assistance from bilateral or multilateral donors or devalue. In general, it is better to slowly depreciate rather than suddenly devalue under duress, generating another detrimental shock for consumers and many businesses.

4. Reinvigorate economic development and diversification plans

Authorities in oil-rich countries may want to use this “pause” to plan for the future, especially those that are historically poor at long-term investments in infrastructure and education. Governments could use this opportunity to improve their medium-term development plans, focusing on energy transitions and supporting economic diversification. One small example is Trinidad and Tobago’s plan for a USD 7.5 million grant facility for Tobago hoteliers to upgrade their hotel rooms. If unemployment stays high into 2021, as is likely in many countries, governments could use the excess labor to (re)build critical infrastructure, such as high-speed internet, water and sanitation and public transport, to improve competitiveness and quality of life over the long run.

Did the U.K. Miss Out on £400 Billion Worth of Oil Revenue?

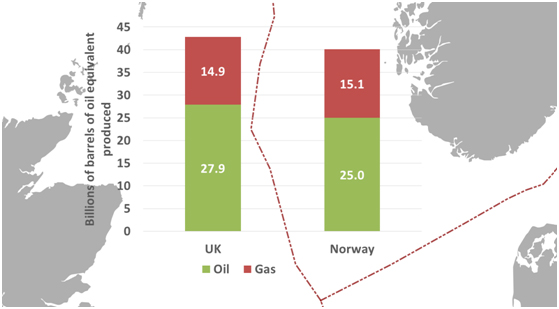

The U.K. and Norway oil and gas sectors provide an ideal comparison through which to compare the outcomes from different approaches to oil sector governance. The two countries have equivalent geology and a similar resource base – the North Sea Basin is effectively split down the middle between them.[1] The U.K. and Norway both began offshore exploration and production in the mid-1960s with the first oil discoveries made in 1969. Since then, both countries have produced similar amounts of hydrocarbons: the U.K. has produced 42.8 billion barrels of oil equivalent (boe) and Norway 40 billion boe (figure 1).

Figure 1. U.K. and Norway oil and gas production since 1971

Source: BP Statistical Review 2014 and Norway government data (www.norskpetroleum.no)

Whilst the geology and resource base in each country is similar, the two countries have taken very different approaches to governance of the sector. Since 1986 the U.K. government has had effectively no direct equity participation in the North Sea and has had a fully private upstream sector, with taxation as the only channel of government revenues from hydrocarbons.[2]

Norway has taken a different approach, with over 50 percent of production coming through Statoil (of which the state owns a majority) and state ownership of assets via the State Direct Financial Interest (SDFI), held through Petoro (wholly owned by the state). Norway generated more than double the revenue the U.K. did from each barrel it produced. The purpose of this article is not to debate whether the current U.K. tax regime is optimal today, but rather examine why the Norwegian approach to oil governance in the past appears to have generated so much more revenue. For other countries seeking to extract more from their resources this case study suggests a valuable lesson: given political stability and competent institutions, a state can have both a relatively high tax burden on its industry and direct ownership of assets, and deliver more revenue for its citizens and still attract investment.

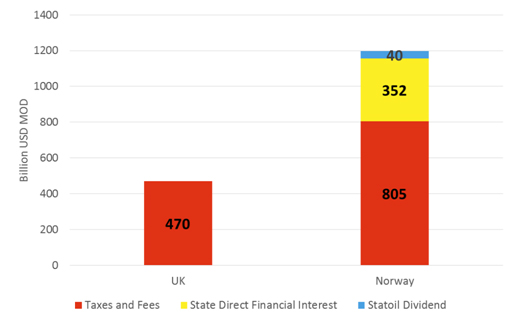

So how much revenue has each country generated from its oil and gas production over the past 45 years? Analysis of official government statistics show that the U.K. generated $470 billion in revenues whilst Norway has generated $1,197 billion since 1971 in real (2014) terms (figure 2).[3]

Figure 2. Government revenues from oil and gas production in real (2014) terms since 1970.[4]

Source: U.K. Statistics of Government revenues from U.K. oil and gas production, table 11.11 and Norway government data (www.norskpetroleum.no).

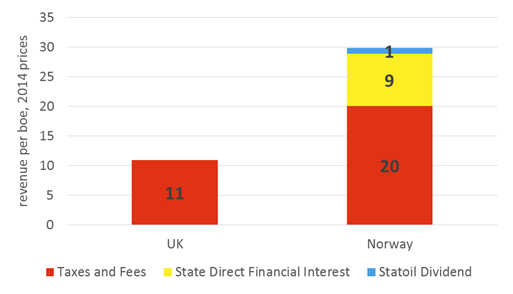

Normalising for production levels shows that the U.K. generated $11.0 per boe compared to Norway's $29.8 per boe in 2014 prices (figure 3). In other words, Norway has generated $18.8 per boe more in revenue for the state than the U.K. has. Figures 2 and 3 show that the difference is due to a combination of $9.1 less tax take per barrel and $9.8 per barrel in state equity cash flow and dividends.

Figure 3. Government revenues from oil and gas production in 2014 prices since 1970 on a barrel per oil equivalent basis

Source: U.K. Statistics of Government revenues from U.K. oil and gas production, table 11.11 and Norway government data (www.norskpetroleum.no).

The $18.8 per barrel extra government revenue Norway enjoyed equates to $727 billion in money of the day terms. On the face of it, this is a staggering sum, equivalent to 35 percent of the U.K.'s national debt stock in 2014.

Not included in these figures is the amount the U.K. state gained from selling its assets in the North Sea. This figure is not precisely known, but accounts suggest that U.K. earnings from the oil company privatisations in the early 1980s were only around £1.2 billion[5] ($1.7 billion) in money of the day terms, or around $3.76 billion in 2014 terms. This is perhaps an underestimate as it does not include income from the privatization of BG beyond its oil assets. Nonetheless, the income to the U.K. from privatization of oil assets does not make up for the lower U.K. government revenues relative to Norway.

Why did the U.K. generate less revenue for the state than Norway from North Sea oil and gas?

Three prominent factors appear to be 1) the timing of U.K. and Norway's production relative to global oil and gas prices, 2) lower average U.K. tax receipts from petroleum production, and 3) the Norwegian state's direct investment in the industry.

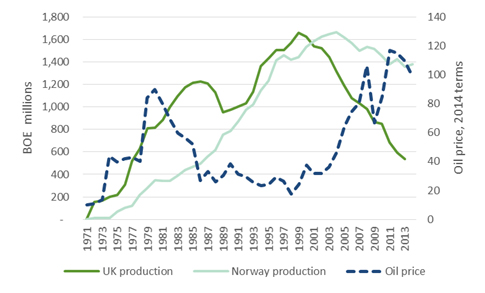

First, U.K. produced more of its oil and gas in years when prices were low than Norway did. The U.K.'s twin peaks of production in the late 80's and late 90's coincided with oil price lows resulting in less rent available to the U.K. state. Norway's production peaked later, in 2004, when oil prices were higher (figure 4).

Figure 4. Oil and gas production and the oil price, in 2014 terms

Source: BP Statistical Review 2014 and Norway government data (www.norskpetroleum.no).

More precisely, the U.K. produced 65% of its oil when prices were below $50 a barrel compared to 57% for Norway. This seemingly small difference in realised sales has meant that Norway sold its oil and gas for about $10 per boe more than the U.K. on average.[6]

Table 1 Oil and gas produced in years when oil prices averaged below and above $50 per barrel in 2014 terms, from 1971

| U.K. | Norway | |||

| Billions of BOE | % of total | Billions of BOE | % of total | |

| below $50 | 27 | 65% | 23 | 57% |

| Above $50 | 15 | 35% | 17 | 43% |

Source: BP Statistical Review 2014 and Norway government data (www.norskpetroleum.no).

Second, Norway earned $9 per boe more just in taxes. Partly this is an effect of the different in timing of sales, as already shown. In part it also reflects the larger field sizes in Norway[7] with consequent lower unit production costs and higher taxable profits. It also reflects differences in the tax regime as Norway has maintained a higher effective tax rate on the oil sector, although these rates have varied over time.[8]

The third factor in the apparent success of Norway has been the involvement of the state. The Norwegian state benefited from direct equity investment in the upstream which generated an additional $9.8 per barrel in revenue. The Norwegian state, via Statoil and Petoro, has majority stakes in 11 of its 14 billion barrel fields. This choice should be weighed against the fact that the Norwegian state risked public money. It is not clear how much this was. SDFI data shows negative cash flow from 1985 to 1988 of $21.4 billion in 2014 terms, but further public capital would have been invested before 1985. In hindsight this was a risk worth taking, but that could not have been known for certain at the time.

These figures suggest that Norway's governance model has been a key contributing factor. Direct state equity in oil and gas production and a higher tax burden has generated significantly higher revenues for Norway, while the British state appears to have failed to gain much value from privatising its North Sea assets.

The U.K. government's decision to end its direct participation in oil and gas equity was controversial at the time. In 1980, the Central Policy Review Staff with the U.K. cabinet office raised the following concerns “Privatising BNOC and selling £1 billion of BNOC's assets benefits the PSBR (public sector borrowing requirement) in the years in which the assets are sold, but the £1 billion gained is purchased at a high price in terms of the PSBR benefits stretching out into the future.” Oil assets “are almost certain to rise in price in the years ahead”.[9]

This warning was prescient as our analysis shows that the U.K. government may have missed out on hundreds of billions of pounds in potential revenue as a result of the privatization path taken in the early 1980s.[10] Emerging oil and gas producers navigating the types of challenges the U.K. and Norway have already faced should take heed.

Keith Myers is the managing partner of Richmond Energy Partners, and a member of the Natural Resource Governance Institute (NRGI) advisory council. David Manley is an economic analyst at NRGI. With thanks to Carole Nakhle and Willy Olsen for their thoughts.

[1] The North Sea accounts for the bulk of U.K. and Norway production. The U.K. also produces from the West of Shetlands and Norway has production in the Norwegian and Barents Sea

[2] Following the privatization of BNOC (BritOil 1982) and The British Gas Council's oil assets (Enterprise Oil 1983) and gas assets (BG 1986)

[3] Official U.K. and Norway government data has been converted to US dollars at the prevailing exchange rates of the time, and adjusted for US inflation using data from the World Bank national accounts database via Index Mundi.

[4] Taxes and fees include standard business taxes, environmental and petroleum specific taxes, royalties and fees. The State Direct Financial Interest is the net return to the Norwegian State on its direct ownership interest in companies operating in Norway. This was started in 1985. Prior to this date, the State managed its interest via the state the owned company Statoil. After 1985, the State's ownership interest was split: one part managed as the SDFI, and one part by Statoil. When Statoil was publically listed, the responsibility for managing the SDFI was transferred to a state-owned management company called Petoro. The Statoil Dividend is the total dividends paid by Statoil to the state as the sole shareholder from 1982 to the present, it does not include net income from 1972 when Statoil was founded.

[5] Britoil £549m, Enterprise Oil £392m, Wytch Farm £210m. Source: David Parker. The official history of privatization Vol 1 1970-1987. Routledge 2009.

[6] The average annual price of sales weighted by production has been $47 per boe for U.K. and $57 per boe for Norway.

[7] 67 percent of Norway's production has been from large fields (over one billion boe), and 17 percent from small fields (between 0.5 and 1bn boe). In the U.K., 23 percent of production has come from large fields and 26 percent from small fields. Source: Richmond Energy Partners.

[8] In terms of the tax take per dollar of sale weighted by production, Norway has received 16 cents more than the U.K.. Authors' estimate based on analysis of U.K. Government statistics, and Nakhle, C. (2008) “Petroleum taxation. Sharing the oil wealth: a study of petroleum taxation yesterday, today and tomorrow”, Routledge Studies in International Business and the World Economy.

[9] David Parker. The official history of privatization Vol 1 1970-1987 Routledge 2009

[10] For a commentary on the policy implications and supporting analysis see Boué, J. C and Wright, P. “Chapter 2. A requiem for the U.K.'s Petroleum Fiscal Regime” in Rutledge, I. and Wright, P. (eds) U.K. Energy Policy and the End of Market Fundamentalism. 2011. Oxford Institute for Energy Studies.