Extracting Emissions: Why Resource-Rich Countries Should Cut Emissions from Extractive Operations

-

Global efforts to mitigate climate change are likely to greatly reduce demand for fossil fuels over time. Countries that depend on revenues from these resources should diversify their economies.

-

Investors and customers are pressuring the oil, gas and mining industries to cut greenhouse gas emissions from their production processes. This trend is likely to intensify, including with new policies from key trading partners seeking to reduce greenhouse gas emissions from the extractive commodities that they import. Examples of such measures include the European Union’s Carbon Border Adjustment Mechanism and its regulations on methane emissions from oil, gas and coal operations.

-

To stay competitive, governments of resource-rich countries will need to cut emissions from oil, gas and mining operations in their territories. Some are already doing this. But progress has been slow, and much work remains. To improve results, a wider set of stakeholders than just governments and including civil society actors should engage on the issue and seek increased transparency and accountability on emissions from the extractive industries.

Introduction

On 1 October 2023, the European Union launched the transitional phase of its “Carbon Border Adjustment Mechanism” (CBAM) through which the EU will tax products of the most polluting industries coming into the EU in proportion to greenhouse gas emissions involved in their manufacture. While the CBAM doesn’t yet apply to raw extractive commodities, it does apply to processed metals and mineral products such as aluminum, cement, fertilizer, iron and steel. And the EU is considering extending the CBAM to cover metals more broadly and refined oil by 2030.

The CBAM’s introduction, as well as the EU’s recent announcement that it will regulate methane emissions from oil, gas and coal operations (including in non-EU countries that export to the bloc), is part of a growing trend whereby investors, downstream industries and governments of resource-importing countries pressure the oil, gas and mining sectors to cut emissions from their operations. Here we analyze this trend and how resource-rich countries can respond to it.

We find that countries producing the extractive commodities that pollute the most (whether from extraction, supply chains or final consumption) will find it increasingly difficult to be competitive as the world prioritizes lower-emission varieties. Governments in such countries should therefore analyze emissions from their countries’ extractive operations. Moreover, officials should a) take this into account when deciding whether to invest further public financial resources in these industries given likelihood of decreased demand for high-emission commodities, and b) cut emissions from the production process as this will be an important factor in the economics of extraction going forward.

Climate change mitigation and resource-rich countries’ economic models

The extractive industries and the commodities that they produce are the main contributors to climate change. The use of mined products, especially the burning of coal, including by the extractive industries themselves, accounts for 28 percent of global greenhouse gas emissions; and burning oil and gas accounts for around 33 percent of total emissions.1

Cutting the use of fossil fuels is therefore essential to fighting climate change and efforts to do so will likely have major impacts on fossil fuel producing countries in the medium to long term. If countries follow through on pledges to cut greenhouse gas emissions, this will mean that oil, gas and coal demand will fall, posing problems for resource-rich countries where economic models depend on the production of fossil fuels. Indeed, many analysts think that global oil demand has already peaked. These dynamics make it imperative for fossil fuel producing countries to diversify their economies.

But demand for and production of fossil fuels is not disappearing overnight, and their climate impact is not limited to their end use. Producing, processing and transporting oil and gas (i.e., the sector’s scope 1 and 2 emissions) accounts for 10-13 percent of worldwide greenhouse gas emissions2 (compared to 2-3 percent from mining). Fossil fuel producers are therefore also under pressure to cut emissions from the production and supply of fossil fuels.

What are scope 1, 2 and 3 emissions?

The three different “scopes” relate to the different ways that extractive companies (or a specific project or the sector more broadly) can cause greenhouse gas emissions.

- “Scope 1” emissions are those that the company causes directly, e.g., through burning fossil fuels or failing to stop leaks of greenhouse gases from its infrastructure.

- “Scope 2” emissions are those that the company causes indirectly through purchases of electricity, steam, heat or cooling (e.g., they could come from fossil fuels that were burned to produce electricity that the company purchases).

- “Scope 3” are the emissions caused by the use of the products and services that the company sells to others. For an oil company, this would include the emissions caused by eventual burning of the fuel produced by the oil company, e.g., in a car or airplane.

Impacts of increasing carbon prices on producing countries

Across the world, governments, customers and investors are all increasing pressure on the extractive industries to reduce emissions from their operations and from their products. These efforts include the rise of carbon pricing, through which governments apply financial penalties to companies/individuals for their greenhouse gas emissions , and discourage the use of fossil fuels. For example, from 2018 to 2021, countries accounting for 80 percent of global energy use increased their average carbon price by around 17 percent. And World Bank data suggest that carbon prices increased further in 2021 and 2022.

This continues a long-term trend. From 2012 to 2018, carbon prices and the share of emissions that they covered had also increased. And an increasing number of countries (e.g., Canada, Norway, EU members) plan to bring in new carbon prices, or increase existing ones. As noted above, the EU’s CBAM even extends the EU’s carbon prices to cover emissions that occurred outside the EU during the production of the bloc’s imports of certain products. This could leave mineral-rich countries exporting to the EU worse off. As one of us has argued elsewhere, such countries should consider implementing their own carbon prices, both for the wider benefits they carry and to eliminate or reduce payments to the EU under the CBAM and potentially under the similar schemes being considered by Canada, the U.K. and the U.S. (though not necessarily with the same sectoral coverage).3

Increased carbon prices could further reduce demand for fossil fuels, leading to a lower market price which in turn could make many oil and gas projects unprofitable. Higher carbon prices will put most pressure on producers of the dirtiest fuels—coal, but also heavier, more carbon-rich oils, the burning of which generates the most emissions, requiring the highest payments of carbon prices, when compared with other fuels. Extra-heavy oils are estimated to emit at least 24 percent more CO2 when burned than light oils. Projects that are both high-cost (meaning that the commodity costs more per unit to extract) and highly carbon-intensive may struggle to be competitive in the future. Governments should therefore be wary of investing public money into development of such projects.

Importance of reducing emissions from extractive operations for future investment and revenues

While measures in extractives-importing countries such as the EU’s CBAM do not currently target emissions from the process of getting the imported oil, gas and minerals out of the ground in the first place. this could soon change. For example, the International Energy Agency and the OECD have called for fossil fuel importing countries to adopt standards on leaks of methane from extraction of the oil and gas that they import.4

The European Union has decided to leverage its position as the largest importer of oil and gas to reduce supply chain emissions of methane from the fossil fuels that the bloc imports. To do so, it will oblige countries from which it imports oil, gas and coal to apply the same monitoring, reporting and verification requirements that fossil fuel producers inside the bloc will have to meet. The European Union will also set a maximum methane emission intensity to the oil, gas and coal that it uses starting in 2030. EU member states will have the power to fine importers who do not respect these limits and monitoring, reporting and verificaiton measures. The bloc is also looking to coordinate this approach to methane emissions with other fossil fuel importers. Such approaches could make it harder for producers with the highest levels of methane leaks to achieve a high market price for their fossil fuel exports (unless they are able to reduce these leaks). Governments in producing countries should act to cut emissions from their extractive industries now, instead of leaving it too late and seeing exports suffer once importing countries implement such measures and producers scramble to make changes.

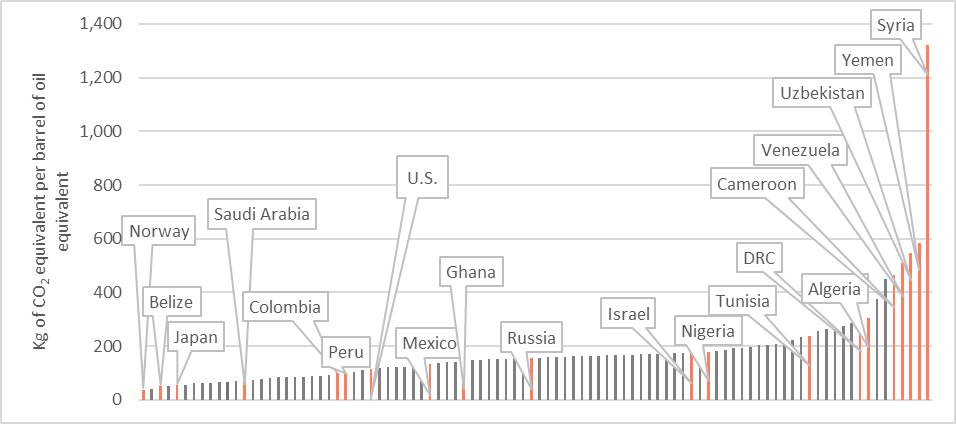

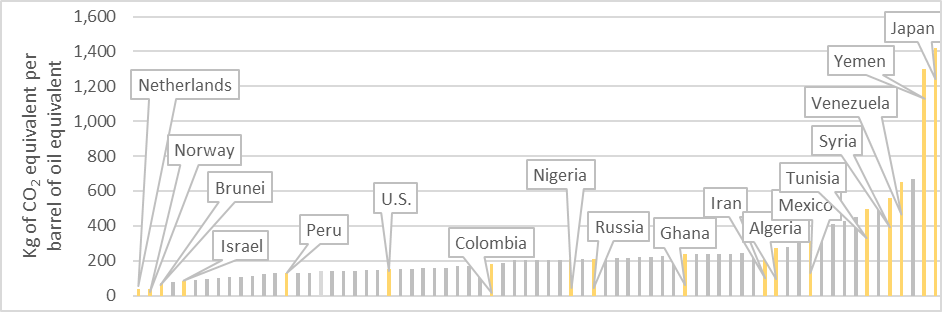

Similarly, investors and customers are pressuring the extractive industries to clean up or lose business or investment. Analysts consider low-carbon oil, gas and mining projects more likely to receive funding than higher-emission projects. And over the longer term, institutional investors expect high-emission oil and gas projects to no longer be viable. Even though for most countries, the bulk of the emissions from their oil and gas comes from burning the fuels upon end use, differences between countries’ supply chain emissions from producing oil and gas vary significantly, as shown in figures 1 and 2 below.5 ,6 These variations in supply chain emissions can add significantly to total emissions (supply chain plus end use) as well. Based on estimates from the Global Registry of Fossil Fuels, total emissions per barrel of oil from countries with the highest supply-chain emissions (top 25 percent) are over 60 percent higher than oil from countries with the lowest supply-chain emissions (bottom 25 percent). The equivalent figure for gas is over 90 percent.

Figure 1. Estimated emissions from oil supply chains7 ,8

Figure 2. Estimated emissions from gas supply chains9 ,10

NB: Yellow bars indicate countries where NRGI has programs and/or are highlighted for other reasons (see footnote 7 for an explanation).

Emissions can also vary significantly between projects in the same country, so some projects within a country may be “competitive” in terms of emissions, while others are not.11

In some cases, policymakers may be able to close this gap. For example, according to McKinsey, the oil and gas sector can reduce its operational emissions by over half at an average cost of less than $50 per ton of carbon dioxide equivalent in greenhouse gas emissions, which may be commercially viable for many projects. Methane accounts for 46 percent of emissions from oil and gas operations. It can be particularly strategic to focus on cutting methane emissions because of the gas’s potency–over a 20-year time horizon, it warms the climate 80 times as much as CO2. This is especially the case because existing technologies can already cut methane emissions from oil and gas production by 70 percent; and around 40 percent of methane emissions from oil and gas could be cut at no net cost by capturing and selling gas that would otherwise be wasted.12 It is also the main source of greenhouse gas emissions from mining; techniques exist to cut methane emissions from that sector too.

To date, a key issue holding back efforts to cut methane emissions has been that companies have lacked incentives to bring them down; even if the cost of cutting methane emissions can be recouped through savings, the “return on investment” may be insufficient to encourage companies to do so. For projects that are not very profitable and cannot afford to bring operational emissions down from a high level, ceasing production, and international incentives to do so, should also be considered.

Those resource-rich countries that move first and fastest to decarbonize their extractive sectors may acquire an edge. This may be particularly true for those with newer facilities that can be designed for low emissions intensities from the start, rather than having to retrofit old infrastructure. For fossil fuel producers, this may help them to be among the “last producers standing” as the world cuts the use of fossil fuels, with importers buying from those sources with the lowest emissions.

Resource-rich countries’ efforts to decarbonize extractive operations

In response to the dynamics identified above some resource-rich countries are starting to cut emissions from their extractive industries.

For example, one of the main sources of emissions from upstream extractives is gas flaring (see above for an explanation) which accounts for around 10 percent of the total emissions from oil and gas production, processing and transport.13

Colombian national oil company Ecopetrol reduced flaring steadily from 2012 to 2021, achieving an estimated 60 percent reduction in flared gas per barrel produced. Colombia has also adopted a specific regulation to cut methane emissions from the sector in 2022. Governments in 10 of the 12 countries where NRGI operates programming have committed to contribute to cutting global methane emissions by 30 percent by 2030.14 In addition, Mexico committed to spend USD 2 billion to reduce methane emissions from oil and gas exploration by 98 percent. Chile, Colombia and Mexico have also introduced carbon pricing, which should encourage extractive industries to cut the use of fossil fuels in their operations. Companies have also tried to limit the emissions from the planned East Africa Crude Oil Pipeline in Uganda and Tanzania by powering it with solar energy (though substantial environmental issues remain).

Roles for civil society and other stakeholders

Much work remains for those seeking to reduce emissions from extractive industry operations. Notwithstanding various stated commitments of companies and governments, and international pledges of financial and technical support, progress has been slow or otherwise disappointing. For example, in Nigeria, although gas flaring substantially decreased between 2000 and 2012, the level of flaring per barrel of oil produced barely changed after that, despite a commitment from the government in 2016 to eliminate routine flaring by 2030.15 ,16 And as international oil companies sell off their most-polluting assets, these have sometimes been bought by companies with lower environmental standards, leading to higher emissions.

Increased transparency and accountability will be important in ensuring greater engagement with the issue and to push governments, companies and investors to take the necessary action. At the international level, the Extractive Industries Transparency Initiative (EITI) has taken an important step, with the revised EITI Standard encouraging extractive-sector companies to publish project-level greenhouse gas emissions from oil, gas and mining projects. This will help governments and citizens assess which projects are most at risk of becoming uncompetitive due to high emissions and how to respond.

At the national level, more effective engagement by a broader set of actors can “move the needle” on emissions from extractive operations. This engagement will be more likely if stakeholders understand that reducing emissions from extractive sector operations is not just about countering climate change, but also related to other national priorities such as protecting government revenues and reducing harms to the health and environment of local communities. With that orientation, civil society, local community groups and concerned citizens can push governments (and businesses) to sufficiently prioritize emissions minimization, including by strengthening the regulatory framework and its enforcement. Looking beyond climate change at this broader set of reasons to cut extractive sector emissions can also increase civil society interest and capacity to campaign effectively on the issue of extractive sector operations emissions. This broader engagement will be important for resource-rich countries to effectively respond to the increasing challenge to cut emissions from extractive operations.

Acknowledgements

The authors would like to thank Paul Bagabo, Lee Bailey, Fernanda Ballesteros, Tengi George-Ikoli, Antonio Hill, Alexandra Malmqvist, David Manley, Valérie Marcel, Juliana Peña Niño, Rob Pitman, Thomas Scurfield, Ricardo Troncoso, Daniel Wilde and Nicola Woodroffe for very helpful comments.

Notes

-

1

Authors’ analysis based on “Greenhouse Gas Emissions from Energy Data Explorer”, International Energy Agency, 2 August 2023, www.iea.org/data-and-statistics/data-tools/greenhouse-gas-emissions-from-energy-data-explorer. And Hannah Ritchie, Max Roser, and Pablo Rosado, “CO₂ and Greenhouse Gas Emissions,” Our World in Data, 2020, ourworldindata.org/co2-and-greenhouse-gas-emissions.

-

2

Authors’ calculations based on Hannah Ritchie, Pablo Rosado, and Max Roser, “Greenhouse Gas Emissions,” Our World in Data, 2020. And “Oil and Natural Gas Supply,” IEA, 2022, www.iea.org/reports/oil-and-natural-gas-supply. Quoted in African Natural Resources Management and Investment Centre, Minimising Greenhouse Gas Emissions in the Petroleum Sector: The Opportunity for Emerging Producers (Abidjan, Côte d’Ivoire: African Development Bank, 2022), 14, www.newproducersgroup.online/wp-content/uploads/2022/11/Minimising-Greenhouse-Gas-Emissions-in-the-Petroleum-Sector.pdf.

-

3

In order to ensure greater international equity in the energy transition, authorities in countries implementing schemes such as the EU’s CBAM should include, in or alongside such schemes, measures to mitigate their negative effects on low and middle-income countries, e.g., through financial and/or technical assistance to help such countries green their economies.

-

4

Methane is a common by-product of oil extraction and a particularly potent greenhouse gas. In the process of getting oil and gas out of the ground, it is commonly emitted either through leaks or planned release into the atmosphere – either unburned (“venting”) or burned (“flaring”). Processing (e.g., refining) and transporting oil and gas also generate significant emissions. See “Methane from Oil and Gas Production Explained,” The World Bank - Global Gas Flaring Reduction Partnership, accessed 24 October 2023, www.worldbank.org/en/programs/gasflaringreduction/methane-explained.

-

5

The Global Registry of Fossil Fuels is an “[O]pen-source database of oil, gas and coal production and reserves globally, expressed in CO2-equivalent… It contains data from 139 fossil fuel producing countries, which amounts to 99% of fossil fuel production aggregated to the national level.” The database also provides estimates of the emissions from producing oil and gas in 91 oil producing countries and 71 gas producers. See “Global Registry of Fossil Fuel Emissions and Reserves”, Global Registry of Fossil Fuels, accessed 4 September 2023, fossilfuelregistry.org.

-

6

Figures 1 and 2 show a selection of countries, including some of the world’s larger oil producers, some of the world’s lower emitting producers as well as a selection of countries where NRGI operates. This is intended to provide reference points to explore whether individual countries will be more or less “carbon-competitive” than other producers based on current intensities and identifying potential examples of good practice among lower emitting producers. We also include a selection of higher-emitting producers, which may provide examples of practices to avoid.

-

7

Source: “Carbon Intensity in the Fossil Fuel Supply Chain”, Global Registry of Fossil Fuels, 2023, fossilfuelregistry.org/carbon-intensity. Global Warming Potential (GWP) 20 is applied to methane emissions; see “Methane and Climate Change,” IEA, accessed 4 September 2023, www.iea.org/reports/methane-tracker-2021/methane-and-climate-change. The impact would be smaller if we used Global Warming Potential 100. The impact over the next 20 years is important and sufficient to justify action on cutting upstream emissions (and using GWP 100 would fail to show this); this is why we have chosen to display GWP 20 in this figure and figure 2. For further discussion, see Janos Maté and David Kanter, “The Benefits of Basing Policies on the 20 Year GWP of HFCs” (Greenpeace, 2011), ozone.unep.org/system/files/documents/Benefits%20of%20Basing%20Policies%20on%2020%20GWP%20of%20HFCs.pdf.

-

8

The world’s largest oil producers are the United States (accounting for 21 percent of global production), Saudi Arabia (13 percent) and Russia (10 percent). See “Frequently Asked Questions (FAQs) - What Countries Are the Top Producers and Consumers of Oil?”, U.S. Energy Information Administration (EIA), 22 September 2023, www.eia.gov/tools/faqs/faq.php?id=709&t=6.

-

9

Source: “Carbon Intensity in the Fossil Fuel Supply Chain.”

-

10

The world’s largest (fossil) gas producers are the United States (accounting for 25 percent of production), Russia (17 percent) and Iran (6 percent). See “Natural Gas Production”, Enerdata World Energy & Climate Statistics - Yearbook 2023, accessed 4 September 2023, www.doi.org/yearbook.enerdata.net/natural-gas/world-natural-gas-production-statistics.html. And Statista Research Department, “Natural Gas Production Worldwide from 1998 to 2022”, Statista, 29 August 2023, www.statista.com/statistics/265344/total-global-natural-gas-production-since-1998.

-

11

RMI provides data on supply chain emissions by oil and gas project. See RMI, “Assessing Global Oil and Gas Emissions”, Oil Climate Index plus Gas, 2023, ociplus.rmi.org.

-

12

Some initiatives to capture methane emissions can have a positive net present value for companies. See Chantal Beck et al., “The Future of Oil and Gas Is Now: How Companies Can Decarbonize,” McKinsey & Company, 7 January 2020, www.mckinsey.com/industries/oil-and-gas/our-insights/the-future-is-now-how-oil-and-gas-companies-can-decarbonize.

-

13

Authors’ calculations based on Tomas de Oliveira Bredariol and Christophe McGlade, “Fossil Fuels,” IEA, 11 July 2023, www.iea.org/energy-system/fossil-fuels. And Tomas de Oliveira Bredariol and Christophe McGlade, “Gas Flaring,” IEA, accessed 15 September 2023, www.iea.org/energy-system/fossil-fuels/gas-flaring.

-

14

This is a 30 percent cut relative to 2020 levels.

-

15

Authors’ analysis based on Rebecca Schulz, Christophe McGlade, and Peter Zeniewski, “Putting Gas Flaring in the Spotlight,” IEA, 9 December 2020, www.iea.org/commentaries/putting-gas-flaring-in-the-spotlight. And “Nigeria,” The World Bank, June 2022, flaringventingregulations.worldbank.org/nigeria.

-

16

In 2022 Nigeria’s government “[I[ssued guidelines to support the elimination of routine gas flaring by 2030 and a 60 percent reduction in fugitive methane emissions by 2031.” “Methane Abatement,” IEA, accessed 2 October 2023, www.iea.org/energy-system/fossil-fuels/methane-abatement.

Authors

Amir Shafaie

Legal and Economic Programs Director