El gran negocio de prestar a Pemex, bomba de tiempo

As Mexico Votes, State Oil Company Pemex Needs a New Direction

In less than two weeks Mexicans will vote for their next president. The outgoing leader, Andrés Manuel López Obrador, has made energy sovereignty and self-sufficiency one of the sustained themes of his presidency. AMLO, as he is universally known, has focused his energy aspirations on Pemex, the world’s most indebted national oil company. What Mexico’s next president does with Pemex will determine the country’s energy and fiscal future amid a rapidly changing outlook for fossil fuels.

Pemex faces unprecedented risk brought about by the quickening global energy transition away from hydrocarbons. At NRGI, we have described that risk in a new Spanish-language report, and summarize it below. We also offer some recommendations for the victor in June’s elections and the Pemex executives, including its director, whom the new president will appoint.

A risky business

National oil companies (NOCs) account for 55 percent of the world's oil production and yet they are moving more slowly than their private sector counterparts in terms of decarbonization planning.

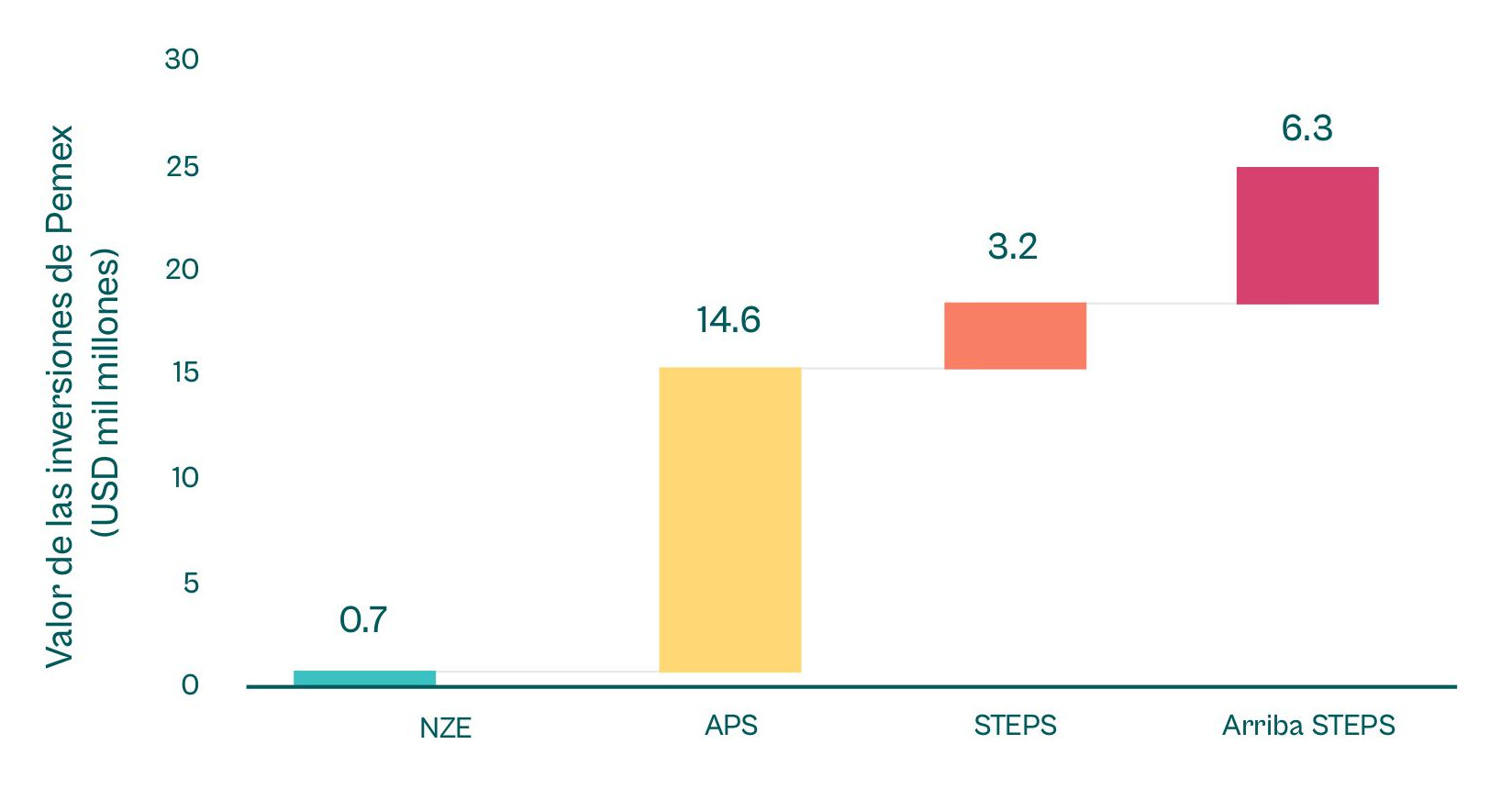

Among the 58 NOCs we studied last year, Pemex ranked 11th in terms of its exposure to transition risk. The biggest of these risks is the changing economics of the oil sector, with demand likely to markedly diminish in coming decades as countries seek to meet their emissions reduction goals. Mexico’s remaining oil reserves will be increasingly costly to extract, meaning that as global oil prices fall, Pemex may be caught out, its assets “stranded.” We found that approximately $10 billion in Pemex's expected investment over the coming decade would not break even under the International Energy Agency’s Announced Pledges Scenario for future oil demand. Given Pemex’s already problematic debt obligations, this presents the government with the specter of more bailouts to alleviate the company’s financial situation, generating an even deeper crisis.

Value of Pemex's upstream oil and gas investments breaking even in each of the IEA's scenarios.

In late 2022, Pemex presented a new business plan which, for the first time, explicitly referenced the energy transition. The plan recognized as risks the international hydrocarbon market contraction due to the increase in electric vehicles, and the downward trend in the demand for oil-derived plastics. While this recognition was an important first step, we still know little about what government officials and Pemex executives plan to do with respect to the transition.

In March 2024 Pemex released a sustainability plan that included more detail on some aspects of its intentions to reduce production emissions. But the plan did not address the transition risk in terms of falling global demand and prices.

Early dissemination of our findings in a workshop with climate and energy experts in Mexico yielded more insight:

- Pemex’s diversification plans remain somewhat vague, and their technical feasibility is uncertain.

- Pemex must be more transparent and accountable about its financial situation.

- Many sector insiders believe that the transition will be slow, and that Pemex will remain competitive.

We are confident that experts from Mexico’s oil and gas sector and its climate community can work with Pemex to improve understanding and communication of its plans.

How to improve Pemex’s future

Our research and consultations have led us to propose three categories of recommendation:

1. Pemex should further recognize and analyze transition risks.

This means more thorough scenario planning around market conditions, shared publicly. And Pemex officials should include more acknowledgement of transition risk in their financial reporting—not just in planning.

2. Pemex should adopt and adapt transition risk mitigation approaches from other oil companies.

Executives should look very carefully at large fields with high production costs. Factoring in lead times (7.5 years on average) and changing market conditions, these may not represent the bonanza that some imagine. One such find is the Kante field in Tabasco state; our analysis suggests that increased investment could be a financial misstep. Ambitions around producing more “no matter what” should give way to innovative thinking about Pemex’s potential role in a domestic energy transition.

Regarding diversification and downstream activities, executives have several opportunities. First, Pemex should better coordinate with CFE, Mexico’s state-owned electricity company. Both can play a fundamental role in advancing the energy transition. Leadership should build a coordinated and integrated vision and action plan that defines the role of each company.

Decision-makers must also carefully consider the viability of diversification options. For example, the two leading presidential candidates have been enthusiastic about expansion in petrochemical production. But petrochemicals only account for 12 percent of current oil demand and the global market may soon be oversupplied as many oil companies seek to expand. This presents a risk of overinvestment and therefore warrants caution.

3. Mexico’s next president should oversee key changes in the government’s approach to the oil and energy sectors.

Mexico’s energy ministry (SENER) should assume a transition planning role in which officials consider the transition risk and build synergies among the country’s state-owned energy companies.

Meanwhile, the finance ministry (SHCP) should review the conditions for financial support to Pemex in the interest of fiscal responsibility and transparency in the management of public resources.

Moreover, the state, as Pemex’s owner, has a crucial role in holding the company accountable. SENER, SHCP, the Congress of the Union and the Federal Superior Audit Office determine and supervise the company's ownership policy. These actors should therefore play a role in improving transition-related decision making within Pemex.

Whoever triumphs on 2 June must stop Pemex from making risky bets and have a clear vision for the company—and Mexico—in a world in transition.

Mexico’s risky bets

Learn more about the transition risks Pemex faces with new NRGI research.

Growing resource-backed loans seen threatening oil economy

Transición energética puede agravar crisis de Pemex y generar una en México: NRGI

Avoiding $1.6 Billion in Debt and Making Fossil Fuel Transitions in Ghana

- In July 2021, the Ghana National Petroleum Corporation stated its intention to spend USD 1.65 billion of public money to purchase a share of undeveloped offshore oil projects held by Aker Energy, a Norwegian company.

- NRGI provided technical analysis to an alliance of civil society actors interrogating GNPC’s request, and raised questions around the value of the asset, GNPC’s capacity to jointly operate the field, and the riskiness of the investment, building on prior NRGI research including Risky Bet. This underpinned advocacy by the alliance calling for investigation and greater transparency around the transaction.

- Following persistent advocacy, the Ghanaian government reduced the value of assets in the Aker-GNPC transaction from $1.65 billion to $1.1 billion and committed to further evaluating the deal. Media investigations revealed that Bank of America had appraised the oil field’s value at $300 million.

- In May 2023, Aker returned ownership of the two offshore blocks to the Ghanaian government for a sale price of $1.

Building partnerships for united advocacy and reform

The extractive sector contributes significantly to Ghana‘s economy. Gold mining has been important for the country for over a century, and Ghanaians have more recently hoped that the country’s oil and gas assets will contribute to public revenues.

Following Aker Energy’s 2017 acquisitions in Ghana of the South Deep Water Tano (SDWT) block and a 50 percent stake in the Deep Water Tano / Cape Three Point (DWT/CTP) block, the Norwegian company dominated the policy environment. It successfully lobbied the government of Ghana to amend the governance architecture of the upstream sector. But more recently, Aker had been seeking private buyers for its stake in these offshore blocks, with no success.

NRGI and many others considered a public investment in the declining oil industry to be a risky bet

In July 2021 Ghana’s national oil company, the Ghana National Petroleum Corporation (GNPC), stated its intention to purchase a share of Aker Energy’s offshore oil projects, after Aker had failed to find any takers. The Minister of Energy submitted a memo to parliament requesting $1.65 billion for the government to finalize negotiations and acquire a 37 percent stake in DWT/CTP and a 70 percent stake in SDWT. NRGI and many others considered a public investment in the declining oil industry to be a risky bet—an accelerated energy transition would reduce the financial returns on this investment and purchasing the assets would divert funds away from programs that were potentially more socially beneficial.

NRGI’s research and technical expertise on national oil companies enabled us to support the Alliance of Civil Society Organizations (CSOs) Working on Extractives, Anti-corruption and Good Governance. We analyzed public data related to the GNPC-Aker transaction, GNPC’s past transactions, its strategic position, and emerging implications of energy transition on Ghana’s oil sector, revenue flows and economy. Concerns arose about the asset’s value, the capacity of GNPC to take on production, and the investment risk amid the transition.

NRGI provided vetted data and technical support to the allied CSOs who were then able to professionally and meaningfully engage on the issues with different stakeholders including the Ministry of Energy, parliament, GNPC, the International Monetary Fund, the World Bank, the Norwegian embassy, the media and the Ghanaian public.

Through an extensive advocacy campaign the alliance called for a halt in the transaction and for the development of a national policy on energy transition. Specifically the alliance (including NRGI) requested that the parliament fully investigate the transaction to verify the actual cost incurred by Aker to date on the blocks, clarify inconsistencies in the presentations by GNPC to Ghana’s cabinet, and allow for open consultation to provide opportunities for independent expert opinions. Alliance members engaged with the media locally and internationally, authored articles, participated in public forums, and called for government transparency regarding the deal. NRGI provided technical support for the development of communication materials and clear infographics for engaging the public. Two press statements were released in 2021 by the CSO alliance—in August and September. These were widely featured in the media in Ghana and abroad.

After 18 months of persistent campaigning, Aker Energy wrote to relinquish its interest in the SWDT block to Ghana for free. This reinforced the CSOs’ position on the risks of investment. In May, 2023 Aker Energy sold the other field to Africa Finance Corporation Equity and Investment for a token price of $1 after the former defaulted on repayment of a loan of $200 million from the latter.

Driving the energy transition agenda in Ghana

In response to the CSO advocacy demands and emerging issues, the Ghanaian government constituted the National Energy Transition Committee (NETC), hosted at the Ministry of Energy. The committee is tasked with developing an energy transition plan to inform a policy for the country and mandated to conduct a nationwide consultation with various stakeholders including CSOs and youth. GNPC and the Ghanaian government officials credited the work of NRGI and the alliance of CSOs as significant influences on the evolution of their approach and requested NRGI’s technical assistance in the development of an energy transition plan.

NRGI continues to advise GNPC and has met with company officials to provide technical support on their plans for developing a comprehensive strategy for diversification in response to the energy transition. Discussions have also addressed the importance of reviewing the law establishing GNPC to understand the governance challenges, the role of government and hindrances to a smooth transition.

In November 2023, NRGI published two reports that reference Ghana and GNPC’s exposure to transition risk—Riskier Bets, Smaller Pockets and Facing the Future—leveraging data in its National Oil Company Database.

Oil’s endgame will be in the Gulf

Facing the Future: What National Oil Companies Say About the Energy Transition

-

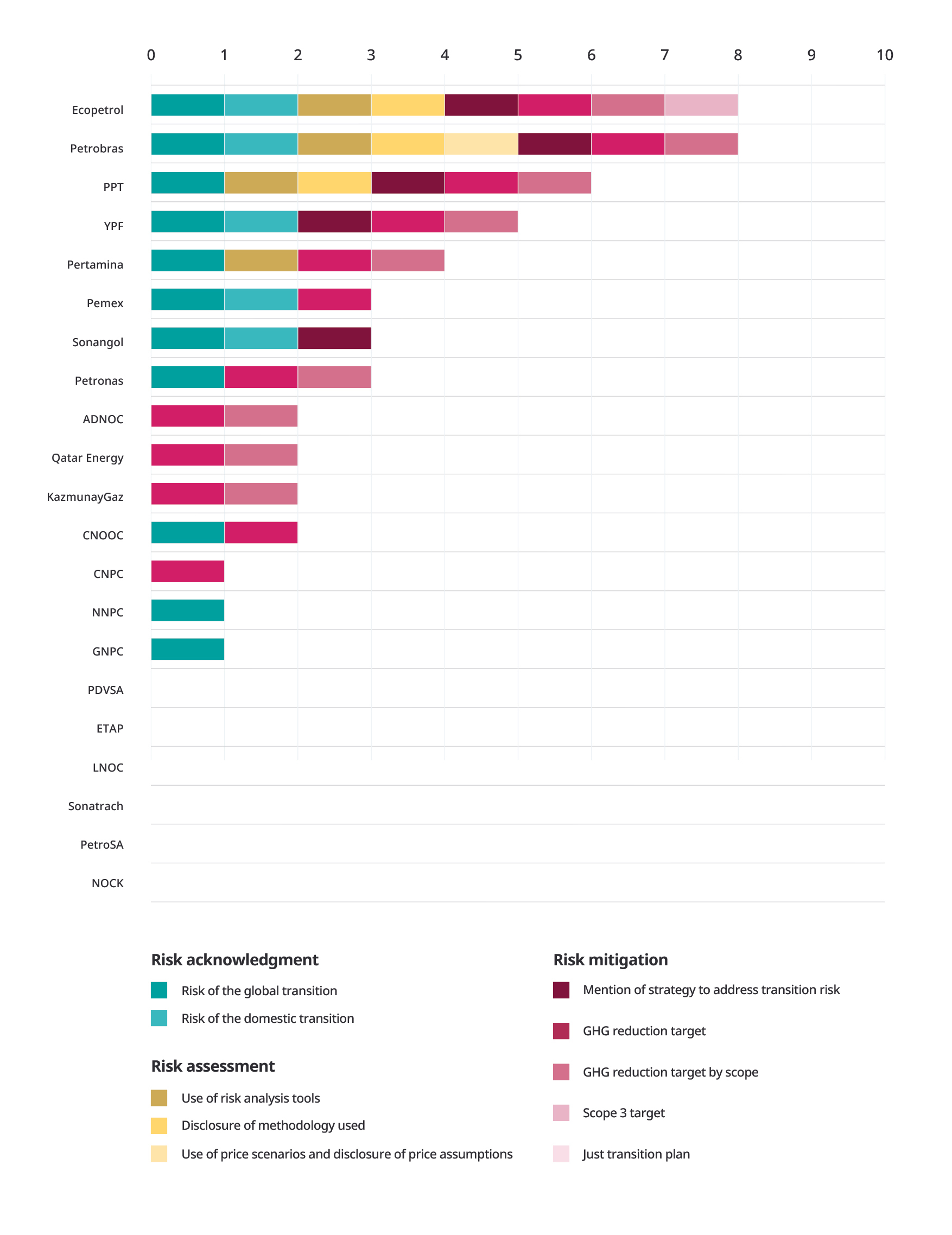

National oil companies (NOCs) should publicly acknowledge the risk of the energy transition, assess this risk, and act by implementing mitigation plans.

-

Only 9 out of 21 NOCs analyzed acknowledge the risk of the energy transition, 4 have mentioned the use of transition risk assessments, and 5 have explicitly mentioned strategies to mitigate the risk.

-

None of the NOCs have published “just transition plans” detailing how they will help workers and communities.

-

NOCs do not plan to decrease investments in risky oil and gas assets. Petrobras (Brazil), Petronas (Malaysia) and Sonangol (Angola) are divesting from less valuable assets, but not necessarily to mitigate transition risk or downsize operations.

-

Some NOCs, such as NNPC (Nigeria) and GNPC (Ghana), want to expedite drilling before oil and gas demand falls and acquire assets divested by other companies.

-

At least six NOCs intend to increase oil and gas investment to secure energy supplies.

-

Most NOCs intend to diversify, especially into gas, oil refineries, petrochemicals and renewable energy. However, it is unclear how much NOCs are spending on diversification or whether these are effective mitigation strategies.

-

NOCs can learn from each other. Two NOCs—Ecopetrol (Colombia) and Petrobras—are clear leaders in terms of recognition of energy transition risk. However, NOCs disclosing more transition risk information are not necessarily also those reducing higher-risk investments.

NOCs’ readiness to manage energy transition risk (based on public statements)

National oil companies (NOCs) produce half of the world’s oil, yet only recently have climate organizations considered NOCs a worthwhile area for advocacy.

Riskier Bets, Smaller Pockets: How National Oil Companies Are Spending Public Money Amid the Energy Transition

-

Expecting a slow energy transition away from fossil fuels, national oil companies (NOCs) will likely invest USD 1.8 trillion in upstream oil and gas developments and expansions over the next 10 years.

-

But $425 billion—a quarter of the NOCs’ planned investment—will be unprofitable if oil demand falls to 55 million barrels a day, in line with the International Energy Agency’s Announced Pledges Scenario. This is the highest risk portion of the portfolio and has doubled since the Russian invasion of Ukraine.

-

NOCs will only profit from around $1.2 trillion of investment (71 percent of the total NOC investment) if humanity fails to contain global temperature rise to below 1.5°C, pushing the world toward climate catastrophe.

-

While NOCs are making riskier bets, their debt is rising in some regions. Between 2011 and 2022, the average debt to total asset value of NOCs in sub-Saharan Africa, the Middle East and North Africa, and Latin America rose by a third.

-

Governments’ financial pockets are shrinking. Between 2011 and 2021, the average government debt as a proportion of gross domestic product doubled.

-

Yet many NOCs have not publicly acknowledged the growing risks of the energy transition. They and their governments must examine how they can generate sufficient revenue and energy for citizens without making even riskier bets with public money.

As the energy transition accelerates and government finances deteriorate national oil companies (NOCs) are gambling their countries’ wealth.

As NOCs, along with the rest of the oil industry, expect oil demand to stay high, they will likely invest USD 1.8 trillion in new upstream developments and project expansions over the next 10 years. However, $425 billion of this investment is unlikely to be profitable if global oil demand falls from the current 100 million barrels a day to 55 million barrels a day by 2050, in line with the International Energy Agency’s Announced Pledges Scenario. This is twice the investment NOCs were planning in 2021 before the Russian invasion of Ukraine. In addition, NOCs will likely invest $1.2 trillion in projects that will only break even if humanity fails to keep the global rise in temperatures below 1.5°C, pushing the world toward climate catastrophe.

Even if demand persists, the future is not business-as-usual for NOCs and their governments. Continued burning of fossil fuels will result in further climate damage to nature, societies and economies: a 13 to 29 percent fall in gross domestic product (GDP) for non- OECD countries by mid-century. Nine out of the ten most affected economies have NOCs. Governments should examine how this radically increases uncertainty and challenges the roles of NOCs and the public capital they are investing.

NOCs in China, Saudi Arabia, Russia and Brazil are set to spend the most. In particular, Chinese and other Asia-Pacific NOCs are increasing their investments significantly compared to their plans two years ago. Conversely, NOCs in Latin America, Eurasia and sub-Saharan Africa are reducing their investments.

NOCs in Sub-Saharan Africa, Asia-Pacific and Eurasia are generally the most exposed to risk. A third of all NOCs—including Indonesia’s Pertamina, Nigeria’s NNPC and Mexico’s Pemex—are due to invest more than a third of their investment pipeline in projects that would not break even under the IEA’s Announced Pledges Scenario (APS). A scenario in which governments meet their climate pledges to reduce oil and gas demand. Some smaller NOCs are highly exposed: four-fifths of Uganda’s UNOC and Cameroon’s SNH investment pipelines fail to break even in the APS.

NOC debt is rising in some regions. Between 2011 and 2022, the average debt to total asset value of NOCs in sub-Saharan Africa, the Middle East and North Africa, and Latin America rose by a third.

NOCs’ investment in risky assets represents a large portion of state budgets—with significant consequences for governments’ ability to fund public services in the future. UNOC and NNPC are due to invest an amount equivalent to more than 30 percent of their governments’ annual expenditure in projects that do not break even in the APS. QatarEnergy and Mozambique’s ENH are also betting large amounts relative to their governments’ budgets, but their focus on gas may reduce their risk exposure.

Value of all NOCs’ aggregate “investment pipelines” measured in 2021 and 2023, by scenarios in which they break even

Responsible Change: How Governments Can Address Environmental, Social and Governance Challenges When Petroleum Assets Change Hands

-

As the world moves toward a future beyond oil and gas, petroleum assets will change hands, with different kinds of companies replacing others.

-

Since 2014, around USD 88 billion in assets have moved from publicly listed to private companies. The roles of sub-Saharan African and Latin American companies in their home countries have expanded.

-

Globally, the role of national oil companies (NOCs) is growing. NOCs have acquired around $24 billion in assets from non-NOCs since 2014.

-

The growing role of private and local companies and NOCs potentially gives producer countries greater control over their petroleum sectors, including the pace of an eventual phaseout.

-

However, these companies often have less capacity and fewer transparency, environmental, social and governance commitments than publicly listed international companies. This increases the risk that these companies’ operations will negatively impact the environment and communities, and that they will be unable to pay for decommissioning when production ends.

-

Many assets that sub-Saharan African and Latin American NOCs have acquired appear vulnerable to energy transition risks.

-

Governments should exercise approval rights over asset transfers to ensure buyers have requisite capacity to operate with high standards. They should ensure transparency to allow host communities and the public to better understand transfer impacts and how the government and/or companies will manage them, and strengthen regulations to address key issues arising from transfers including emissions management and reporting, and decommissioning funding.

-

Governments should require NOCs to make adequate disclosures about their acquisitions to ensure NOCs manage risks to the public purse.

As the world journeys towards a future beyond oil and gas, oil and gas assets will continue to change hands, with different kinds of companies filling the gap left behind by others.

There is growing concern that, as international oil companies (IOCs) face pressure to reduce emissions, they are selling upstream petroleum assets, in part, to shift emissions off their books and ostensibly achieve their decarbonization goals. On balance and at a global level, assets are moving from publicly listed to private companies and from companies with higher environmental commitments to those with weaker commitments. The result, according to some evidence, is that these sales do not simply transfer emissions to new parties but may increase them.

At the same time, some national oil companies (NOCs) seek to acquire assets left behind by the departure of IOCs to avoid production decline and ensure domestic energy supply.

This briefing shows how asset transfer trends may differ by region and country, and therefore present different risks and raise different policy considerations for producer country governments. It focuses on the Global South countries and regions in which the Natural Resource Governance Institute (NRGI) works.

NRGI analyzed upstream petroleum asset transfers from 2014 to the first half of 2023, using Rystad data to identify trends globally, at the sub-Saharan African and Latin American regional level, and in NRGI’s countries of focus.

This analysis shows that petroleum assets worldwide have moved primarily from publicly listed to private companies during the period studied. Since the start of 2014, around USD 88 billion in assets have moved from publicly listed to private companies. Both sub-Saharan Africa and Latin America have seen net divestment by publicly listed companies. In sub-Saharan Africa, there has been a transfer of around $23 billion in assets from publicly listed to private companies since the start of 2014, while in Latin America, around $11 billion in assets has moved from publicly listed to private companies.