Santa Marta: Real Progress, and a Gap That Cannot Be Ignored

This week, the Governments of Colombia and the Netherlands hosted the first global conference dedicated to transitioning away from fossil fuels, which ended with real progress—but also at least one critical absence. The Santa Marta conference put the many perspectives of Global South producer countries, subnational communities and the human stakes of energy transitions more clearly on the agenda. But, in a significant omission, national oil companies (NOCs) were neither present nor discussed at the level required given their significance to the transition away from oil and gas.

NOCs already produce more than half the world’s oil and gas (with that share expected to rise), and that they represent the economic backbone of many producer countries; failing to include them and/or the barriers and solutions to their transformation undermines the prospect for roadmaps to deliver a fair, orderly, and equitable transition.

An NRGI delegation was in attendance, and we will be sharing further analysis in the weeks ahead. Today, we are sharing some of our top-line reactions:

For the first time, Global South producer realities were centered

"Santa Marta opened up an important conversation about what is at stake for Global South producer countries—energy independence, less instability, more inclusive and equitable development—and brought in voices that are often missing, like subnational governments," said Ana Carolina González, NRGI's Senior Director for Programs and Latin America Director.

For the first time, a major international forum placed the realities affecting communities in Global South producer countries at the center of the transition debate: fiscal dependence on oil and gas revenues, the instability that comes with price volatility, and what it will take to ensure the shift away from fossil fuels works for the people most affected by it. Importantly, subnational governments had a seat at the table. In many oil-producing regions, the transition is not a future concern—it is already arriving. In the oil producing regions of Campeche in Mexico or Putumayo in Colombia production has declined significantly. Where royalties account for 70–80% of local budgets, like in Niger Delta, a drop in production can mean schools with fewer teachers, roads that go unrepaired and workers facing an uncertain future. These are the communities that contributed least to the climate crisis. They should not be the ones absorbing its costs.

With conflict in the Middle East fueling oil price spikes and energy security fears, the current crisis made the case for an orderly transition stronger. As González put it: "For producer governments, high prices may create pressure to double down on fossil fuel investment. But volatility is not stability and short-term gains are not long-term strategy. The window to plan an orderly transition is open—the question is whether governments use it."

National oil companies: a missing piece

The co-host takeaways noted that participants "stressed the importance of clear policy signals and long-term planning, including clearer strategies for State-Owned Enterprises." At the final press conference, Colombia's Minister of Mines and Energy Irene Vélez Torres acknowledged that NOCs "should be part of the roadmap, because this is where the production takes place. So we hope that the countries can think about how their own companies should be included and should have targets of transition."

These are welcome signals. But recognizing that NOCs need clearer strategies is not the same as bringing them in as essential partners, and the gap between limited acknowledgement and meaningful inclusion is where credible transition planning can break down.

"NOCs are not peripheral players," says González. "They produce more than half of the world's oil and gas and that share projected to rise to 62% by 2050. NOCs are the economic backbone of many producer countries. The next step must bring them in as essential partners in any credible transition roadmap."

In many producer countries, NOCs underpin national budgets, jobs, public services and local economic stability. In Colombia, Ecopetrol alone contributed the equivalent of around 11% of the national budget in 2023, more than the country allocated to the education sector. Pemex directly employs over 128,000 people, with oil dominating the economy of states like Campeche, where it accounts for the vast majority of local economic activity.

Around $400 billion in planned NOC investment between 2023 and 2032 may not break even if demand falls in line with climate commitments. In some countries, more than 80% of planned investments are at risk. Leaving NOCs outside transition planning does not protect them or the economies that depend on them—it simply means the risks accumulate without a strategy for managing them. NRGI's recent report, NOC Transformation: Strategic Choices for an Uncertain Energy Future, offers a practical framework for how governments and NOCs can navigate this moment together.

What comes next

The co-host's takeaway note from Santa Marta does recognize that “clearer strategies for State-Owned-Enterprises" (which include NOCs) are important for long-term transition planning. The conclusions of Santa Marta will now feed into COP31, with Brazil’s COP30 presidency committed to building on the outcomes from Santa Marta in the roadmap it will deliver to this year’s annual UN climate conference (COP31) in Turkey. The Brazilian COP30 Presidency’s roadmap report cannot leave national oil companies on the sidelines. And, we need to ensure that spaces that meaningfully centre the needs of communities most exposed to the transition become the rule, not a welcome exception. The road ahead is long, but the direction is clearer—and Santa Marta moved it forward.

Beyond Oil and Gas: Regional Perspectives on a Transition Under Pressure

As more than 50 countries gather in Santa Marta for the first conference dedicated to transitioning away from fossil fuels, NRGI's regional directors share how governments are navigating competing pressures, and what this means for economies and communities

The energy transition is happening. It is also, depending on your perspective, too slow, too fast, too expensive, or something else entirely. As the governments of Colombia and The Netherlands convene the first-ever conference dedicated to transitioning away from fossil fuels in Santa Marta, that ambition is running up against a charged reality: oil price spike, land grabs, geopolitical jockeying for resources and mounting debt in many producer countries.

NRGI’s work is grounded in the recognition that how the transition unfolds—and how quickly—will determine whether it contributes to fair, inclusive and more prosperous societies, while acknowledging that communities that have contributed least to the climate crisis too often stand to lose the most. There is not one transition. There are transitions—shaped by very different starting points, economic realities and development priorities. Those gathering in Santa Marta must consider these diverse perspectives, including from communities, countries and regions that are not always fully represented in these debates.

Three of our regional directors reflect on how the transition is unfolding in practice, drawing on two decades of work on resource governance.

How are governments approaching the transition in the current context?

Santa Marta's organizers argue that current conflicts reinforce rather than sideline the case for transition. For governments navigating oil price uncertainty, rising energy demand and immediate security pressures, however, the picture is more complicated.

Africa—Nafi Quarshie, Africa Director

Latin America—Ana Carolina González Espinosa, Latin America Director and Senior Director for Programs

MENA—Laury Haytayan, MENA Director

Pathways for Transformation: What Today’s Energy Uncertainty Means for National Oil Companies

As global energy debates become increasingly polarized, governments are pulling in different directions. Some are advancing plans to transition away from fossil fuels—including Brazil’s COP30 roadmaps process and the upcoming Santa Marta conference organized by Colombia and The Netherlands—while others are doubling down on oil and gas for fiscal stability and energy security. National Oil Companies (NOCs)—which produce more than half of the world’s oil and gas—lie at the heart of these debates and of the choices countries now face.

But beyond political narratives, the energy system is already shifting. For instance, in 2025 twice as much capital flowed to renewables and related technologies compared to oil, coal and natural gas.

And while the conflict in the Middle East has pushed oil prices above $100 a barrel, boosting short-term revenues for some NOCs, future demand remains uncertain, even if it is expected to peak around 2030.

For NOCs, this is a defining moment. Charting a path forward that balances fiscal risk and opportunity, and unlocks inclusive development at this moment of extreme uncertainty is vital—for governments, NOC executives and citizens in oil and gas producing countries.

Our new report, National Oil Company Transformation: Strategic Choices for an Uncertain Energy Future, explores how governments can define transformation pathways that align NOC strategy with national development priorities in an increasingly volatile energy system, building on two decades of experience and country examples.

The future of oil and gas is increasingly the future of NOCs

NOCs produced about 54 percent of global oil and 50 percent of gas in 2025, with their combined share projected to rise to around 62 percent by 2050.

This dominance reflects structural advantages: large, low-cost reserves and sustained investment capacity. In 2025, NOCs spent more than US$240 billion in capital expenditure—more than oil majors (US$73 billion) and independent producers (US$109 billion) combined. As private firms scale back or divest, NOCs are increasingly taking on a larger share of global assets.

This growing role creates opportunity but also risk. What once looked like market leverage—greater control over supply and investment—now increases public exposure in a context of energy uncertainty.

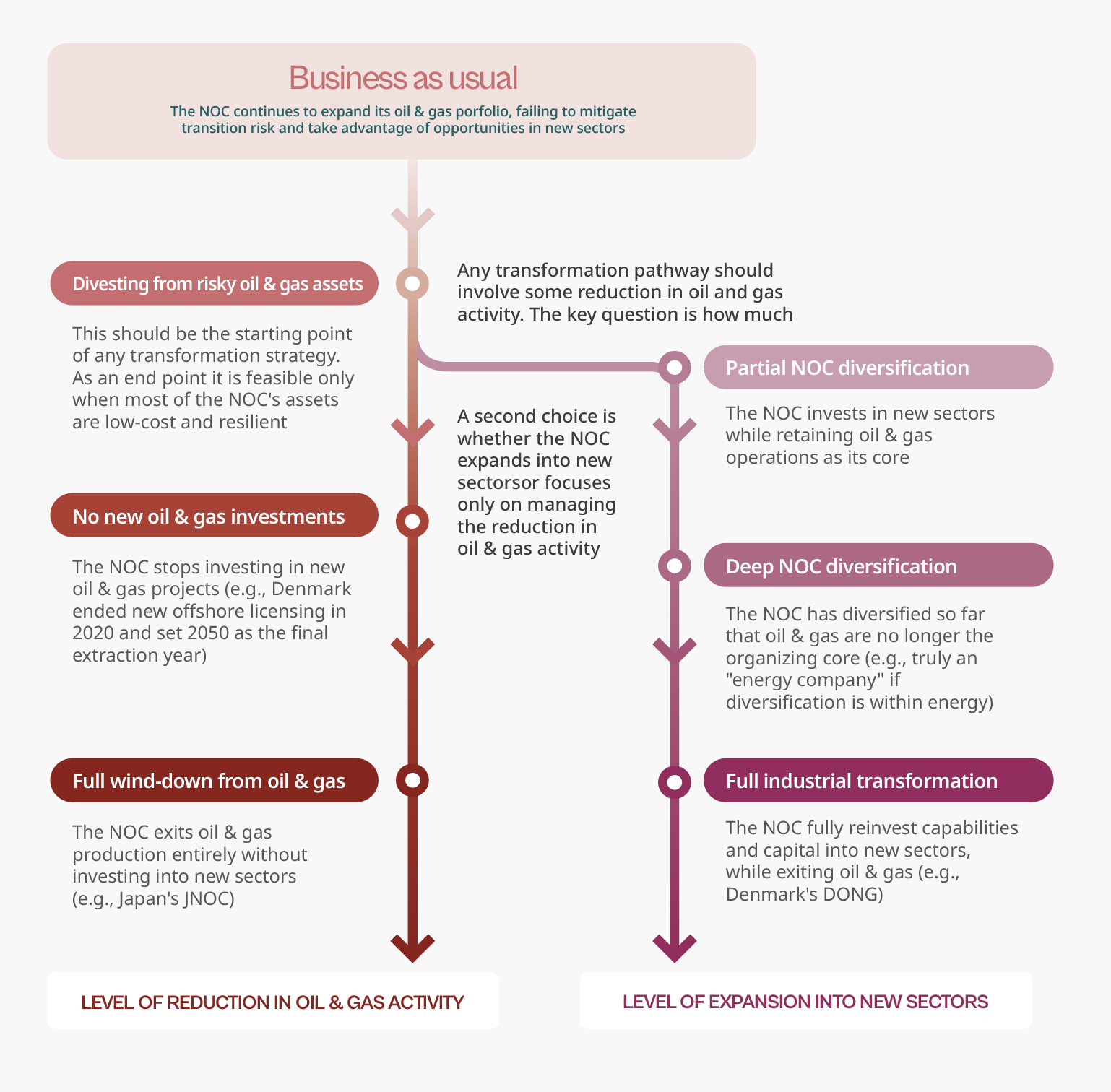

Business as usual is no longer a neutral strategy

NRGI has previously warned that long-lived, capital-intensive oil and gas investments by NOCs risk becoming unprofitable under faster transition scenarios. This risk is already visible. Projects approved under more optimistic demand expectations can generate much lower returns if market conditions turn out weaker.

Recent modelling illustrates the scale of this exposure. As the figure below shows, even under relatively moderate transition assumptions, some NOCs could see projected company value—based on expected future cash flows—decline by more than 50 percent.

This reflects a core challenge: while NOCs cannot control how demand evolves, their investment decisions determine how exposed they are. Unlike oil majors, which face shareholder and legal pressures that can constrain capital allocation, NOCs often operate under political and fiscal pressures to sustain production, revenues and employment, even as uncertainty grows.

For governments that rely on NOCs for development, this makes business-as-usual far from neutral. Asset devaluation at NOCs carries real public costs—weakening balance sheets and shrinking fiscal space for healthcare, education and economic diversification.

When planning for decline is delayed, these risks become harder to manage. The burden often falls on subnational regions and communities through job losses, reduced revenues and limited alternatives.

In this context, short-term gains from high oil prices can mask longer-term vulnerabilities. Uncertainty will shape the sector. The real issue is how prepared countries are to respond.

Why NOC transformation matters now

Vast oil and gas reserves do not translate into development on their own. In some cases, governments have used NOCs to drive more industrial activity and capture more value domestically. In others, weak governance had led to inefficiencies, political capture and fiscal risk.

Today, the stakes are higher. The energy transition is narrowing the window to use hydrocarbon wealth for long-term economic transformation. Delaying decisions about a NOC’s future role risks channeling short-term profits into activities that fail to deliver lasting benefits for citizens before market conditions tighten. At the same time, the opportunity to use these revenues to support diversification and low-carbon transformation pathways may not remain open indefinitely.

NOCs are not a single type of actor. They differ widely in mandates, resource bases, capabilities, governance and exposure to transition risks—and in how they recognize and respond to these challenges.

The question is no longer whether NOCs should transform, but how. What matters is identifying pathways that are fiscally credible, aligned with national development goals, politically feasible, and part of a fair and orderly energy transition. Our new report sets out a practical framework to help governments navigate these choices.

For countries advancing national transition roadmaps, including under the COP30 Brazilian Presidency, NOC reform offers a concrete way to connect climate ambition with fiscal and development strategy. But even for those continuing to invest in fossil fuels, clarifying the future role of the NOC is equally essential to managing long-term risk.

From insight to action

These are decisions countries are already facing—and often without a clear strategy. NRGI’s National Oil Company Transformation: Strategic Choices for an Uncertain Energy Future report provides detailed analysis, country examples and a five-step framework to support policymakers and NOC representatives to navigate these decisions.

Join our webinar on April 21 and hear directly from policymakers and national oil company representatives.

National Oil Company Transformation: Strategic Choices for an Uncertain Energy Future

National oil companies (NOCs) are among the most important actors in the global energy system. They already produce the majority of the world's oil and gas—54 percent of global oil and 50 percent of gas in 2025—and their combined share is projected to rise to around 62 percent by 2050. Significant amounts of public money flow to NOCs1 —in 2025, NOC capital expenditure (US$240 billion) was more than three times that of the oil majors (US$73 billion)2 , and well over a trillion dollars of new investment is expected before 2033.

Beyond these metrics lies another important truth—in many countries, NOCs are deeply entwined in national identity and are often anchor employers for entire communities and regions. They help fund public services, shape national budgets, and support jobs and local economies. In some cases, their decisions affect everything from energy access to infrastructure investments.

Against today’s backdrop of geopolitical turbulence, volatile oil prices and the energy transition, governments face difficult decisions: how to balance near-term revenues with long-term risks, and how to align NOC strategies with broader development goals. (See here for a more detailed exploration of the strategic context facing NOCs). The right choices could see NOCs become engines for inclusive, prosperous societies and critical players in a just energy transition. Conversely, strategic missteps could see NOCs become drivers of waste, corruption, inequality and environmental harm.

Today, NRGI is publishing National Oil Company Transformation: Strategic Choices for an Uncertain Energy Future—a new report that lays out a clear, five-step framework that governments, NOC leaders, civil society and other stakeholders can use to seize new opportunities, minimize risks and define credible transformation pathways. The report is published as NRGI marks its 20th anniversary under the theme “Transforming resource governance for a new era”. We are committed to using the anniversary as a milestone to take stock of what has been learned and to put that knowledge to work on the challenges that will define the coming decades. Few are more consequential than the question of how NOCs navigate the current uncertain environment and the energy transition.

To meet the needs of policymakers, National Oil Company Transformation: Strategic Choices for an Uncertain Energy Future includes country examples and guiding questions to aid the strategic process. The report also pays particular attention to two areas that are often underexplored: assessing transition risk and new business opportunities, and ensuring a just transition and responsible exit.

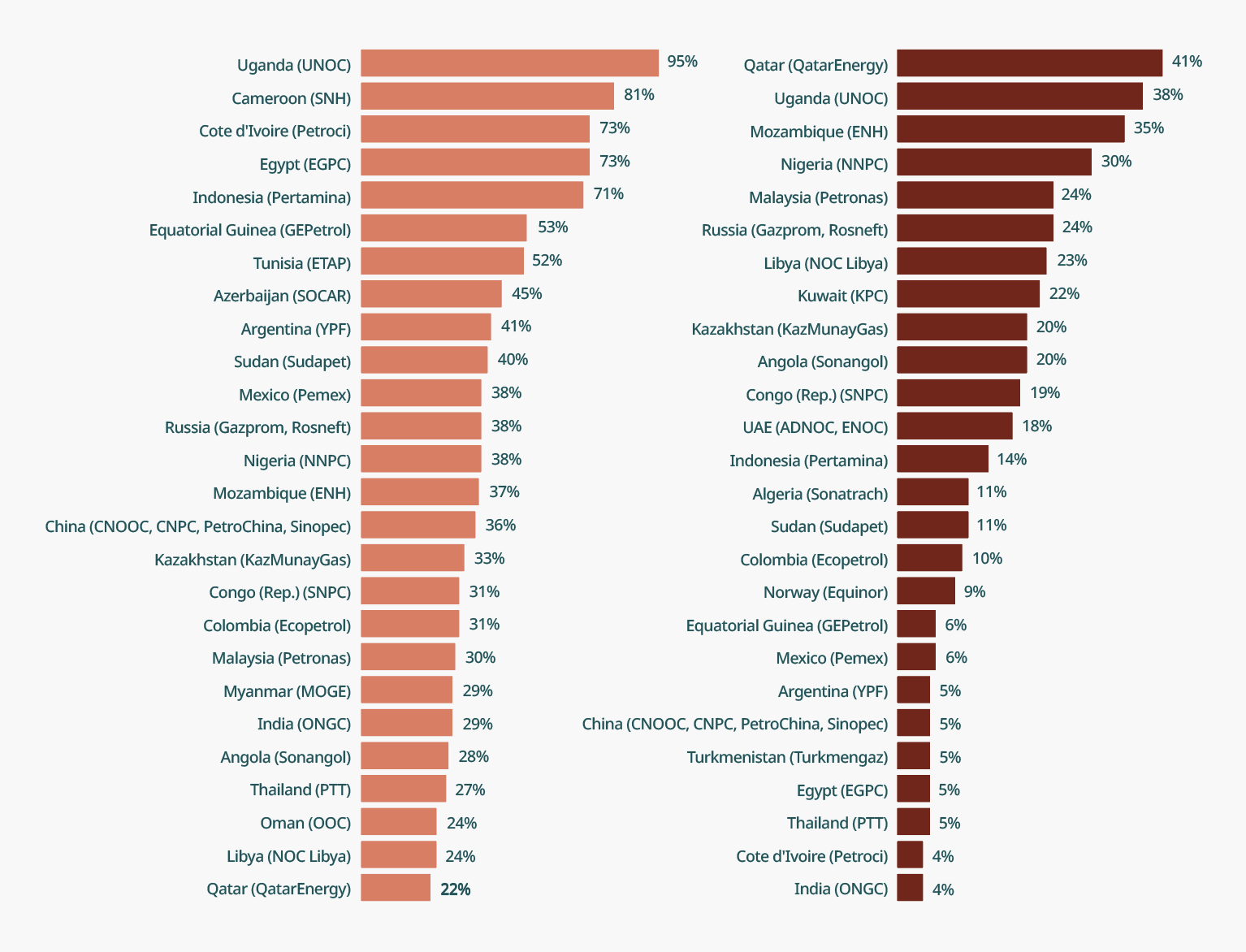

On transition risk, the report shares striking analysis from NRGI’s earlier Riskier Bets report. NOCs face sharply different levels of exposure—from Uganda's UNOC and Cameroon's SNH, where more than 80 percent of planned investments may not break even under plausible transition scenarios, to lower-risk NOCs with more resilient, lower-cost portfolios. The report also challenges the assumption that a pivot to gas automatically reduces risk, examining how price volatility, contract structures and rapidly falling renewables costs complicate that picture.

break even under APS (left) and as a percentage of annual government expenditure (right)1

On just transition, the report is equally substantive. NOCs are not only commercial entities—in many producing regions they are anchor employers and service providers, and their transformation carries real consequences for workers and communities. The report draws on emerging practice from NOCs including Petronas, Petrobras and PetroSA to set out concrete strategies for workforce transition, subnational economic diversification and community engagement.

The report is clear that there can be no "one-size-fits-all" model. Policymakers must make difficult trade-offs with the well-being of all of a country’s citizens in mind, and the framework is designed as an entry point for structured dialogue rather than a prescriptive blueprint.

The report is equally clear that business-as-usual is not a neutral option. Amid structural shifts in energy markets, inaction will expose countries to rising fiscal, social and political risks. NRGI’s Riskier Bets analysis showed that under a scenario in which governments meet their existing climate pledges and global oil demand falls accordingly, around 25 percent of planned 2023–2032 upstream investments across NOCs may fail to break even—with significant consequences for governments and their citizens. Governments and NOCs must act now, proactively reviewing and refining their strategies in response to energy transition pressures and opportunities. We hope that this report is both a spur to action and a practical tool for change.

Download the report today, and register for a webinar on 21 April during which we will unpack the report in more detail, and hear directly from policymakers and NOC executives on how they are meeting this moment.

If you want to connect with NRGI to learn more about our work on NOCs, you can reach out to Andrea Furnaro

From Transparency to Transformation: NRGI’s NOC Work Past, Present and Future

Over the past two decades, national oil companies (NOCs) have moved from the margins of governance debates to the center of discussions to fix how countries manage resource wealth and navigate the energy transition.

NOCs produce more than half of the world’s oil and gas, and in many producing countries their decisions have major implications for public finances, energy policy and long-term development outcomes. That role is only growing in importance in an increasingly uncertain energy future. How NOCs can adapt to that uncertain future remains unresolved, and shocks such as today’s soaring and volatile prices serve as a potent reminder of the need to look ahead and plan for the future.

NRGI’s work on NOCs has evolved alongside these shifts, supporting more informed and inclusive decision-making about natural resources and the energy transition. As we mark our 20th anniversary in 2026, we are building on this experience with new insights on the future of NOCs.

Our new report National Oil Company Transformation: Strategic Choices for an Uncertain Energy Future is part of that effort. As we prepare to launch this work, we are also taking a moment to reflect on how our thinking around NOCs has evolved through four key phases, and what this means for the choices that countries face now and hence for the future of NRGI’s NOC work.

1. Building the foundations: from transparency to governance and country-driven change (2006-2017)

NRGI’s early work focused on extractive revenue transparency, helping citizens better understand how extractive revenues flowed into public coffers. NOCs were not initially central to this agenda, but concerns about country-level corruption risks and NOC opacity gradually brought them to the fore, particularly around their role in financial flows.

Sustained work on NOC oil sales transparency followed and led to tangible impacts. In Nigeria, work by NRGI and partners NEITI led to NNPC canceling criticized contracts. NRGI also produced guidance on state-owned enterprise (SOE) disclosures, supporting global norm strengthening and supporting efforts by organizations such as México Evalúa to assess NOC transparency.

Over time, we expanded beyond transparency to other core NOC governance questions, asking not just what is disclosed, but how institutions are run. This included delving into NOC reforms such as limiting political interference while ensuring sufficient oversight.

In the early 2010s, we also began engaging more deeply on NOCs in emerging “oil hotspots” such as Ghana, including partnering with Chatham House and the Commonwealth Secretariat to establish the New Petroleum Producers Group. Key to our approach was tailoring methods to different settings, balancing cross-country learning with the reality that not all countries are Norway.

Across these early engagements—from UNOC in Uganda to Pertamina in Indonesia—we started to combine cross-cutting NOC research with country-level engagement, and saw this as useful in achieving impact, including in difficult contexts such as Myanmar.

- Effective NOC governance is critical and multi-faceted. NOC transparency is necessary but not sufficient. It must be paired with other governance improvements, including stronger institutions and oversight.

- Real change is largely country driven. Global tools are most impactful when shaped by and applied through country programming, drawing on deep country knowledge and partnerships.

2. Leveraging a data-driven approach for impact (2017-2020)

The second phase focused on data to drive reform, inform decisions, shape incentives and encourage better performance of NOCs.

The Resource Governance Index (RGI) benchmarked more than 50 NOCs and showed widespread governance gaps. This data-driven approach helped lead to tangible changes.

In Qatar, engagement with Qatar Petroleum resulted in the company publishing annual and sustainability plans on its website for the first time. In Mexico, NRGI inputs to the National Hydrocarbons Commission (CNH), whose purview included regulation of Pemex, led to CNH pushing Pemex to improve transparency.

A major milestone in this phase was the launch of NRGI’s National Oil Company Database, the world’s largest open dataset on NOCs. It provides quantitative insights on fiscal transfer patterns and debt-sustainability risks, helping governments, private-sector analysts, journalists and international financial institutions better understand the profound public finance implications of NOC decisions.

NRGI also used this data-driven approach to support country-level analysis of opportunities and risks surrounding NOC oil sales, including in Ghana, and resource-backed loans, including in Nigeria.

Across these efforts, NRGI used data as a lever: to clarify fiscal stakes, justify accountability asks, and strengthen the connection between evidence and reform.

3. NOCs and the challenges of the energy transition (2021-2025)

In this third phase, the energy transition became central to our NOC work, which in turn helped shape broader understanding of the role NOCs play in shaping the global energy transition. In addition to controlling more than half of global oil and gas production, NOCs control around 40 percent of total sector investment and close to 60 percent of reserves.

NOCs play a critical role in how producing countries respond to declining long-term demand for fossil fuels. Their investment strategies can either reinforce continued dependence on oil extraction or support a more diversified energy future.

A major NRGI focus during this phase was on the “risky bets” of NOCs in a context of weakening global hydrocarbon demand. Importantly, NRGI framed these risks primarily as a public investment and fiscal management challenge. We highlighted the impact of NOC investment choices on national cash flows, debt sustainability and long-term fiscal space. This framing proved influential in Ghana where supported partners including the Alliance of Civil Society Organizations (CSOs) Working on Extractives, Anti-corruption and Good Governance to help prevent a risky prospective investment by GNPC.

Recognizing the value of peer benchmarking among NOCs, we assessed how 21 NOCs acknowledge, assess and mitigate transition risks. We complemented this comparative approach with analysis anchored in country challenges, linking transition to fiscal and institutional questions such as Pemex’s debt challenges in Mexico and Ecopetrol’s relationship with Colombia’s government.

During this phase our NOC work also expanded into climate-related areas, including the crucial role of NOCs in methane emissions in Mexico, Nigeria and the MENA region. We contributed to methane abatement finance guidance targeted at NOCs and worked to improve incorporation of NOCs in national climate commitments, including in Mexico. We also worked with partners such as IISD on more effective climate community engagement with NOCs, including at various COPs.

Across countries such as Colombia, Ghana, Mexico, Nigeria, Senegal and Uganda, our work responded to a growing demand among various stakeholders to deepen informed national debate on how NOCs navigate the energy transition.

4. The next phase: NOC transformation

NRGI’s NOC work is now entering an exciting next phase.

With the launch of our new report, we move beyond assessing risk to examining how governments, NOC leaders and other stakeholders can define credible NOC transformation pathways that manage transition risks while making the most of emerging opportunities.

The report sets out a framework to help countries:

- Define national-level policy goals,

- Assess capacities and constraints, including the NOC’s ability to pursue new business opportunities,

- Align mandates, governance structures and financial resources with the chosen transformation pathway, and

- pursue a just transition, given the important role NOCs play in shaping outcomes for workers and communities in oil producing regions.

This framework also reflects a key lesson from our in-country experience: there is no single model. What is feasible, and at what pace, will differ across countries and NOCs. Transformation pathways must reflect fiscal realities, political dynamics and institutional capacity.

Looking ahead

NRGI’s NOC work will continue to evolve to meet new challenges.

We will contribute to discussions on transition roadmaps, where the role of NOCs will be decisive, and to accountability on methane commitments, where NOCs lag significantly behind.

Our NOC transformation work will expand to better include energy security, the financing of transformation and links to national “green industrial policy” plans. We aim to update the NOC Database to integrate transition indicators, strengthening cross-country benchmarking and national advocacy.

This also means engaging more with narratives shaping NOC policies and strengthening strategic communications to better support national debate on NOC transformations.

As highlighted during the launch of NRGI’s 20th anniversary earlier this month, the lessons of the past provide a foundation to “confront the challenges that persist, and the new ones that emerge.” This is particularly true for NOCs. As NOCs take on a larger role in an uncertain energy future, the stakes are rising. The challenge is no longer just improving NOC governance, but defining the role of these companies in addressing the most pressing resource governance challenges—from navigating energy transition risks and opportunities to advancing both development and decarbonization.

NRGI looks forward to continuing this dynamic NOC work with partners to respond to these challenges.

Impact stories

For more on the real-world impacts of NRGI’s NOC work over the years, read the following impact stories:

A Just Energy Transition in Six Oil- Producing Regions: Bringing Local Priorities to Global Climate Action

Colombia, Ghana, Mexico, Nigeria, Peru and Tunisia

Key messages

- Global oil demand is expected to peak by 2030, and all countries—including low- and middle-income producers—will need to transition away from fossil fuels, with richer countries going first. For oil-dependent economies, the imminent peak in demand poses major risks of loss of revenue and jobs, and unintended socioenvironmental impacts, which might be more heavily felt at the subnational level, widening preexisting social and environmental injustices rooted in the fossil economy. Significantly, these risks are already materializing in many oil-producing regions in the global South.

- Yet many national and subnational plans in these countries still overlook how to manage the transition beyond oil, leaving countries unprepared.

- A people-powered, just transition in oil-producing regions could provide the means to address these major equity and justice gaps, while also opening opportunities for people and the planet. It could protect local economies and the rights of those most affected by the decline in oil production: workers in both formal and informal sectors, women, youth, Indigenous Peoples, people with disabilities and the environment.

- A people-powered, just transition in oil-producing regions would allow climate action to be rooted in the demands and needs of local stakeholders, boosting local and national coalitions in support of international agreements, and to influence them.

- National and subnational governments should define comprehensive plans to build fiscal resilience and reduce oil dependency, while ensuring local economies diversify. The visions and priorities of citizens and communities, especially in oil-producing regions, should be included in those plans through participatory processes and multistakeholder dialogue. The international community must provide the technical and financial support needed to help build resilient economic and energy systems beyond oil. Diversification of oil-dependent regions should be part of the just transition agenda.

- National governments, companies and private investors should establish and enforce requirements for a responsible exit in oil-producing countries and regions, involving the active engagement and participation of local authorities and communities. This includes policies and practices around decommissioning, asset transfers, rehabilitation, funds for decommissioning and transition, and socioenvironmental liabilities. Affected communities should be included and compensated, and nature should be protected. A responsible exit should be part of the just transition agenda.

- A just transition in oil-producing regions requires that national and subnational governments, and the international community, provide support to formal and informal workers, women, youth and other often-marginalized groups, to ensure they have the skills and the technical and financial resources to thrive in the process of transitioning away from oil. This means ensuring not only that they benefit from transition policies, but that they have the resources and spaces to be agents for change.

In the current urgent need to address climate change, shifting to clean energy and more sustainable economies is central to the required effort. The energy sector is currently responsible for approximately three quarters of greenhouse gas emissions. In this context, international instruments such as the 2015 Paris Agreement commit countries to “making finance flows consistent with a pathway towards low greenhouse gas emissions and climate-resilient development.”

Most commitments and climate negotiations have focused on emission reductions. However, this started to change with the adoption of the Glasgow Climate Pact at the 2021 United Nations Climate Change Conference (COP26). Countries committed to transition towards low-emission energy systems, “including by rapidly scaling up the deployment of clean power generation and energy efficiency measures, including accelerating efforts towards the phasedown of unabated coal power and phase-out of inefficient fossil fuel subsidies, while providing targeted support to the poorest and most vulnerable in line with national circumstances and recognizing the need for support towards a just transition.”

A people-powered, just transition in oil-producing regions could protect local economies and the rights of those most affected by the decline in oil production.

This was further reinforced at the 2023 United Nations Climate Change Conference (COP28), when governments committed to “transition away from fossil fuels in a just, orderly and equitable manner.” Although further policy commitments have since been difficult to advance, market shifts demonstrate that the transition in fossil fuel demand is already in motion. Technological progress has pushed private investments in the clean energy sector up by 42 percent.

Whether the transition becomes an opportunity for shared prosperity or a source of new inequalities depends on how it is governed.

Yet in several oil-producing countries and regions, these global shifts and their implications are still not widely understood or integrated into policy discussions, and international dialogue and actions do not recognize the needs of local stakeholders in these regions. This also relates to the fact that the increased investment in the renewable energies sector remains unequally distributed—for example, with only 2 percent landing in Africa, due to policy volatility, ineffective financing mechanisms and high capital cost. Yet Latin American countries—especially Brazil, Colombia and Costa Rica—have seen a 25 percent increase in clean energy investments in 2025.

This inconsistency has allowed many oil- and gas-producing countries to remain under the radar in transition debates. The unique challenges and specific needs associated with moving away from oil and gas have not received adequate support. Gaps in research have contributed to a lack of understanding and information about the risks and opportunities for oil-producing regions. More recent research has started to recognize the need for finance to support just transitions in the oil and gas sector, and to move beyond coal. The latest Just Transition Report from the United Nations Framework Convention on Climate Change (UNFCCC) suggests that policy-makers need to address future changes in oil and gas demand. However, processes are not as mature as for coal, and tend to focus on labor and energy access without considering other challenges in producing regions.

This policy brief outlines the critical importance of a just energy transition for oil-producing countries, and identifies risks for local actors, as well as gaps in subnational, national and global policies. It explains how a transition from oil to renewable energy sources can be an opportunity for people and the planet, and provides actionable recommendations to achieve a balanced and equitable approach.

The recommendations of this brief were informed by a mix of desktop research and an in-person meeting in Cartagena, Colombia, in July 2025, with delegates from oil-producing regions in the global South, as well as a meeting during NY Climate Week in September 2025. The brief profiles six oil-producing countries in the global South—Colombia, Ghana, Mexico, Nigeria, Peru and Tunisia—to identify general trends in the transition process, as well as context-specific factors.

National Oil Companies Are Gaining Ground in Climate Talks. Can COP30 Turn Interest Into Action?

National oil companies (NOCs) have long been peripheral to climate debates. But that’s starting to change.

NOCs produce more than half of the world’s oil and gas output, yet they have remained largely absent from climate debates. Unlike international oil companies, they are state-owned actors that shape and are shaped by national policy. In the last COP cycles, however, their presence has grown.

At COP28, 34 NOCs signed the Oil & Gas Decarbonization Charter, pledging to cut operational emissions, end routine flaring and reduce methane intensity to 0.2 percent by 2030. The Charter, however, does not address emissions generated when the oil and gas they produce is burned, and many signatories continue approving new oil and gas projects, patterns inconsistent with the global stocktake’s call to transition away from fossil fuels.

Beyond COPs, climate interest in NOCs is growing. NRGI has received more invitations to speak at climate forums about NOCs and collaborate on the topic. Other organizations are also expanding work in this space, such as EDF on methane measurement and IISD on NOC transition pathways. Yet, despite this momentum, few governments are integrating NOCs into their climate policies.

Most national pledges overlook NOCs

Only ten countries mentioned their NOC in their NDC 2.0 (in any form, including just a passing reference): Azerbaijan, Cameroon, China, Colombia, Ecuador, Oman, Mexico, Qatar, the UAE and Venezuela. In the current wave of NDC 3.0 updates, only five countries have done so to date: Azerbaijan, Angola, Bangladesh, the UAE, and Venezuela.

As state-owned enterprises, NOCs embody the government’s direct influence—and responsibility—over an important source of emissions. For example, in Mexico the energy sector accounts for around 64 percent of national greenhouse gas emissions, and Pemex alone produces about 95 percent of the country’s hydrocarbons.

Countries that have not yet submitted their NDC 3.0 can still integrate them in this round; those that have can incorporate them into implementation frameworks so that climate commitments remain credible.

However, a mention is not a commitment to action. Below are core elements of robust NOC integration into NDCs. To date, only the first category appears in any NDCs.

- Set explicit carbon and methane reduction targets for the NOC.

- Colombia’s NDC 2.0 mentions that “Ecopetrol committed in 2019 to reduce its emissions by 20% by 2030 in line with the country target defined in 2015.”

- Qatar’s NDC 2.0 states that “Qatar Petroleum (QP) is committed to zero routine flaring by 2030, with a long-term goal to reduce flaring in onshore facilities to the absolute minimum.”

- Mexico’s NDC 2.0 notes that “Petróleos Mexicanos has set a methane gas utilization target of 98%, considering the production of existing and new fields.”

- The UAE’s NDC 3.0 mentions the NOC’s ambition “to achieve net zero by 2045” and “reduce carbon intensity by 25% by 2030,” and a target to “have methane intensity below 0.15% by 2025.”

- Express those targets in absolute terms, with defined baselines and reference years.

- Cover full value chain emissions—including Scope 3 emissions—associated with current, planned and projected operations, with clear milestones for national action on Scope 1 and 2.

- Disclose or estimate the NOC’s share of national emissions.

- Explicitly align NOC strategies and capital spending with national climate targets.

- Establish a framework for tracking NOC-specific emissions and progress.

- Acknowledge exposure to transition risks (economic, fiscal and market impacts from a long-term decline in oil and gas demand).

- Task the NOC with contributing to a just transition such as regional economic diversification, workforce reskilling and responsible infrastructure decommissioning.

- Involve NOC leadership and workers in the NDC drafting process.

Why stronger NOC targets could unlock climate finance

International lenders and climate finance institutions increasingly treat NDCs as investment plans. When NOCs are major emitters, they need NOC-specific targets and disclosures. Without this level of transparency, it is difficult to assess investment needs or align climate finance instruments.

Methane reduction is where climate finance can move fastest. Around 80 percent of oil and gas abatement options are cost-neutral or profitable. NOCs could lead the way. With targeted funding for leak detection, flaring reduction and monitoring, governments could secure rapid, measurable results.

For countries like Mexico or Nigeria, where regulations already exist but enforcement is weak, including these targets in NDCs could strengthen oversight and attract international support for implementation.

Climate planning around NOCs must also address just transition responsibilities

The UNFCCC has emphasized that this next round must include the social and economic plans that make emissions targets viable—and this just transition focus is set to increase at COP30. For countries with NOCs, such plans are impossible without them.

In many low- and middle-income countries, NOCs are major employers and fiscal pillars. NOCs also often safeguard national resources and ensure energy security. Their operations are tied to public services, regional development and politics, making them vital actors and potential obstacles to change. For example, Pemex has resisted methane regulation and enforcement efforts, shifted targets and limited independent oversight.

Global just transition agendas, including the UNFCCC’s Just Transition Work Programme, rarely mention NOCs. Recognizing their role is crucial to building just transition strategies that are socially inclusive and politically viable.

In Mexico, oil-dependent states of Campeche and Tabasco are already feeling the effects of declining production—from shrinking fiscal revenues to job losses. Mexico’s climate policy should incorporate explicit just transition measures linked to Pemex’s operations, focusing on regional economic diversification, workforce reskilling and responsible decommissioning of oil infrastructure.

How can COP30 advance the integration of NOCs in climate action?

Brazil—where Petrobras’s role continues to expose the tensions between climate ambition and fossil expansion—offers a key stage to keep NOCs in focus and advance their integration into national climate policies. This means embedding NOCs into national climate frameworks with measurable targets, transparent reporting and clear roles in just transition strategies.

If the right framing and direction are set, COP30 can help governments, investors and climate advocates to embed NOCs into the architecture of climate governance—ensuring that the actors most central to the fossil economy become equally central to its transformation.

Measure to Manage MENA National Oil Companies’ Methane Emissions Reduction Commitments

Key messages

- As methane emissions gain greater global attention and financing becomes increasingly tied to climate performance, the participation of Middle East and North Africa (MENA) national oil companies (NOCs) in global frameworks and initiatives is expected to grow. However, this will likely be at a different pace due to differing capacity and objectives of each NOC in the region.

- NOCs integrated into global financial markets are more likely to participate in multiple international climate initiatives and adopt ambitious. In contrast, isolated NOCs are slower to act unless driven by government mandates or policy priorities.

- NOCs’ methane abatement strategies can differ significantly than those of international oil companies (IOCs) due to differences in their ownership structures, regulatory environments, operational priorities and access to capital and technology.

- Most MENA NOCs operate largely within domestic regulatory frameworks which may be less stringent on methane emissions, especially in developing countries. Often, these NOCs prioritize economic growth and energy security over environmental or climate concerns.

- The lack of consistent and reliable methane emissions data from some NOCs presents a significant barrier to effective abatement. Without accurate baseline measurements, it is difficult to identify priority sources, track progress and evaluate the effectiveness of mitigation efforts. Such data gaps can undermine transparency, making it challenging for stakeholders—including regulators, investors and international partners—to assess performance or offer targeted support.

Executive summary

Methane is a potent greenhouse gas (GHG) and the second-largest contributor to global warming after carbon dioxide, and more harmful in the short term. The global oil and gas industry accounts for nearly one quarter of global methane emissions. National oil companies (NOCs) produce about half of the world’s oil and gas, with one third coming from the Middle East and North Africa (MENA). They play a pivotal role in addressing global methane emissions.

While many climate advocates call for an end to fossil fuel production, producing countries and their NOCs continue to argue that they can maintain production while reducing emissions, mainly through investments in mitigation technologies.

As part of its strategy in the MENA region, the Natural Resource Governance Institute (NRGI) works with governments, oversight actors and NOCs on policies and practices related to a just energy transition. In this context, NRGI commissioned this study to assess the role of seven NOCs in MENA—Abu Dhabi National Oil Company (ADNOC), Saudi Aramco, Petroleum Development Oman (PDO), Iraqi state oil companies, Bahrain Petroleum Company (Bapco), QatarEnergy and Sonatrach—in methane emissions and reduction strategies.

The key findings of this report are:

- There are variations in commitments and capacity: NOCs in the region display varying levels of commitment to methane reduction. These differences are less a function of financial capacity than the result of influences from transparency commitments; technical and human capabilities; and political and economic constraints.

- ADNOC and Saudi Aramco are leaders in measurement and reporting: ADNOC and Saudi Aramco are the most advanced NOCs in the region at monitoring, reporting and reducing methane emissions. Both have access to significant resources and have committed large funds to decarbonization. In 2022, Saudi Aramco launched a USD 1.5 billion sustainability fund, while ADNOC allocated $15 billion to decarbonization projects by 2030, aligned with its net-zero 2050 target.

- Algeria and Iraq are lagging performers: In contrast, NOCs in Algeria and Iraq have shown limited willingness to commit to costly methane reduction initiatives, given their central role in national economies and dependence on oil revenues.

- Access to international debt and equity markets is a key driver of NOCs’ climate commitments. Companies like Saudi Aramco, ADNOC and QatarEnergy, which are heavily integrated into global capital markets, are more responsive to investor pressure and have signed up to international initiatives such as the Oil and Gas Methane Partnership (OGMP 2.0). Conversely, NOCs with little or no exposure, such as Algeria’s Sonatrach, face weaker external incentives to adopt ambitious methane strategies.

- There are emerging shifts: Some NOCs, particularly in Iraq, are beginning to seek external financing for modernization, exposing them to greater international scrutiny and creating opportunities to attract green finance for methane reduction.

Pemex and Mexico’s NDC 3.0: Seizing the Moment for Climate Leadership

A decade after the Paris Agreement, world leaders are convening in New York at the invitation of the UN Secretary-General to announce new targets and measures to address the climate crisis. Mexico took part in this summit, focused on Nationally Determined Contributions (NDCs), the Paris Agreement’s main instrument for reducing emissions and steering the energy transition.

President Claudia Sheinbaum has pledged that Mexico will reach net-zero emissions by 2050. To achieve this, the country’s updated NDC must go beyond technical greenhouse gas (GHG) reduction targets. It should provide a clear roadmap that links climate action to real improvements in people’s lives, including more stable jobs, stronger communities, and a future-ready economy.

In this context, Pemex must play a central role. The energy sector accounts for 64% of the country’s GHG emissions, and Pemex is responsible for 95% of hydrocarbon production and the bulk of associated infrastructure. In Mexico, to talk about hydrocarbons is essentially to talk about Pemex.

Why Pemex?

International experience shows that state-owned oil companies are still unprepared for the challenges of the energy transition, including declining oil demand. Governments have a decisive role to play. By setting clear policy signals and creating financing mechanisms, they can help these companies shift toward new business models.

The Mexican state holds a particularly strong influence over Pemex, given the company’s heavy reliance on government support. In 2025 and 2026 alone, Pemex faces debt maturities of US$24 billion, while the proposed 2026 budget allocates MXN 263.5 billion for debt servicing. That figure is double the 2025 allocation, equivalent to half of the resources earmarked for senior citizens’ pensions and six times the proposed environmental budget.

A stronger, more decisive commitment from Pemex would send a powerful signal that Mexico is willing to align its state-owned company with its decarbonization and just transition goals. Such a step would not only reinforce national climate ambition but also build confidence among the international community, the financial sector and the public.

Integrating Pemex into Mexico’s NDC 3.0: three priorities

1. Reduce methane emissions

Methane is 25 to 80 times more potent than CO₂ and poses serious health risks to communities living near oil facilities. Between 2012 and 2021, Pemex’s largest emission increases came from this gas.

Between 2021 and 2024, Pemex’s methane emissions fell by 29 percent. The company launched its first sustainability plan and voiced its commitment to the World Bank’s Zero Routine Flaring by 2030 initiative. However, Pemex’s methane output remains higher than a decade ago and above that of its international peers. Cutting these emissions is both urgent and strategic, as proven technological solutions exist and, in many cases, are cost-effective. The updated NDC offers the right framework for Pemex to adopt absolute, phased reduction targets, improve measurement and transparency, and join the Oil & Gas Methane Partnership (OGMP 2.0). Doing so would position Mexico as a global leader in methane mitigation.

2. Manage transition risks

Pemex ranks 11th among 58 state-owned oil companies most exposed to transition risks, according to a recent NRGI analysis. Up to US$10 billion in assets could become uneconomic under the International Energy Agency’s Announced Pledges Scenario, posing major risks for public revenues, jobs, and communities tied to the oil industry.

Mexico's updated NDC should respond by promoting transparent risk assessments, redirecting investments toward lower-carbon, higher-return projects, encouraging business diversification, and fostering joint ventures with the Federal Electricity Commission (CFE). It should also establish stronger corporate governance mechanisms under the Ministry of Energy’s (SENER) oversight to ensure planning is consistent with sustainability goals.

3. Just transition plans for oil-producing regions

States such as Campeche and Tabasco, heavily dependent on oil revenues, are already experiencing the impacts of declining production. To ensure no one is left behind, Mexico’s NDC should include just transition plans and the responsible decommissioning of infrastructure. This roadmap should prioritize economic diversification, workforce retraining, tailored educational programs, and greater transparency on environmental and health impacts.

These measures are in line with the outcomes of Mexico’s Local Conference of Youth proposals (2025 LCOY) and the Ministry of the Environment and Natural Resources’ (SEMARNAT) agenda for NDC 3.0, can foster a transition that delivers tangible benefits to the communities most dependent on oil.

Pemex at the center of Mexico’s climate action

The NDC gives Mexico a critical chance to raise its climate ambition, demonstrate international leadership, and put Pemex on a sustainable path. Explicitly including the company would send a clear signal of commitment to a just and orderly transition, in step with the global call to move beyond fossil fuels.

For decades, Pemex has been at the center of Mexico’s energy policy. It must now be at the heart of its climate response. This is the moment to show that commitment and accelerate progress toward net-zero emissions by 2050, building a more equitable, transparent future that delivers for all Mexicans.

Pemex y el sector privado: un diálogo sobre los riesgos y las oportunidades

Ciudad de México, México

En un momento crucial marcado por la transición energética y el inicio de una nueva administración gubernamental en México, líderes de la industria se reunirán durante dos días para analizar los retos y las oportunidades del sector en Mexico Oil & Gas Summit 2025.

Fernanda Ballesteros, Gerente de País de NRGI en México, moderará el panel El próximo capítulo de las asociaciones Pemex-privados, donde se explorará en profundidad la evolución de la relación entre Pemex y los actores privados, así como sus implicaciones para el futuro energético de México.

El panel tendrá lugar el miércoles 24 de septiembre, de 10:15 a 11:30 horas, y contará con la participación de expertos:

- Fluvio Ruiz, experto en Energía

- Alma América Porres, ex Comisionada de la Comisión Nacional de Hidrocarburos (CNH)

- Antonio Escalera, Consultor Senior de Tethys Energía

- Manuel Cervantes, Socio Fundador de MCM Abogados

- Sergio Pimentel, director Jurídico de Jaguar E&P

- Jorge Anaya, vicepresidente de Servicios Legales y Comerciales de Harbour Energy

No te pierdas esta conversación clave sobre el futuro de la colaboración en la industria petrolera y gasífera de México.

Con la participación de

Fernanda Ballesteros

Mexico Country Manager